Are you thinking about tapping into your home’s value but aren’t sure whether a home equity loan or a mortgage is the better choice for you? Making the right decision can save you thousands and protect your financial future.

This guide will help you understand the key differences, benefits, and risks of each option so you can choose the one that fits your needs perfectly. Keep reading to discover which option can work best for your situation and how to make your money work smarter for you.

Home Equity Loan Basics

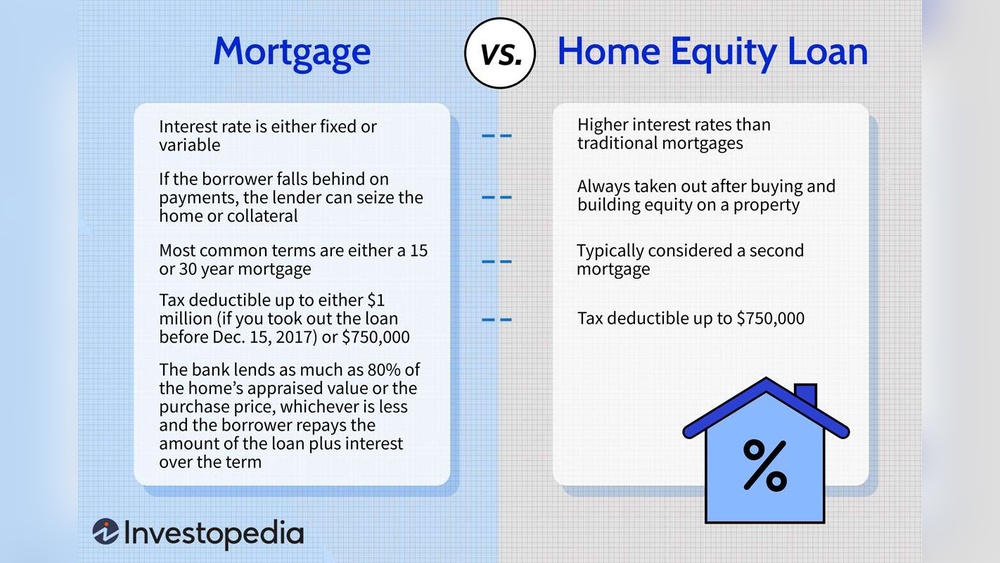

Home equity loans let homeowners borrow money using their house value. The loan amount depends on the home’s current market value minus what is owed on the mortgage. These loans often help with big expenses like repairs or debt consolidation. They offer a way to get cash without selling the home.

Understanding how home equity loans work helps decide if they fit your financial needs. These loans have fixed interest rates and set terms. Borrowers repay the loan in monthly payments over time. The loan uses the home’s equity as collateral.

How Home Equity Loans Work

Home equity loans let you borrow a lump sum. The lender uses your house as security. The loan amount is based on your home’s equity. You repay with fixed monthly payments. The interest rate stays the same for the loan’s life. The loan term usually lasts from 5 to 30 years.

Typical Terms And Rates

Loan terms often range between 5 and 30 years. Interest rates are usually lower than credit cards. Fixed rates mean your payments stay stable. Rates depend on credit score and market conditions. Typical rates may range from 4% to 10%. Closing costs and fees can apply.

Credit: www.experian.com

Mortgage Essentials

Understanding mortgage basics is key before choosing between a home equity loan or a mortgage. Mortgages help you buy a home or refinance debt. They involve borrowing money that you pay back over time with interest. Knowing mortgage essentials helps you make smart financial decisions.

Mortgages come in many forms. Each type has its own rules about payments and interest. Learning these types makes it easier to pick the right one for your needs.

Types Of Mortgages

Fixed-rate mortgages keep the same interest rate throughout the loan. Monthly payments stay steady, which helps with budgeting. Adjustable-rate mortgages start with a low rate. After a few years, the rate can change based on the market. Interest-only mortgages let you pay only interest at first. Later, you start paying the loan’s principal. Government-backed loans like FHA or VA offer lower down payments and easier credit rules. Each type suits different financial situations.

Interest Rates And Terms

Interest rates affect how much you pay monthly and total cost. Lower rates mean less interest paid over time. Loan terms usually range from 10 to 30 years. Shorter terms have higher monthly payments but less total interest. Longer terms lower monthly payments but increase total interest. Knowing your budget helps you choose the right rate and term. Rates can be fixed or variable, affecting payment stability.

Comparing Costs

Comparing costs is key when choosing between a home equity loan and a mortgage. Both have different fees and payment structures. Understanding these differences helps you save money and avoid surprises. Let’s break down the main cost factors.

Upfront Fees And Closing Costs

Home equity loans usually have lower upfront fees than mortgages. You might pay for an appraisal and application fee. Some lenders charge closing costs on home equity loans, but they tend to be less than mortgage closing costs.

Mortgages often include several fees: appraisal, credit report, title insurance, and origination fees. These can add up to thousands of dollars. Some lenders offer no-closing-cost mortgages, but those costs may increase your interest rate.

Monthly Payment Differences

Monthly payments for home equity loans are generally fixed. You pay the same amount each month for the loan term. This can make budgeting easier.

Mortgage payments can be fixed or adjustable. Fixed-rate mortgages keep payments steady. Adjustable-rate mortgages start low but can rise later. Mortgages usually have longer terms, so monthly payments might be lower but last longer.

Interest rates for home equity loans tend to be higher than mortgage rates. This means monthly payments could be higher on home equity loans.

Credit: www.chemungcanal.com

Risk Factors

Choosing between a home equity loan and a mortgage means understanding the risks. Both affect your finances and home ownership differently. Knowing these risks helps you make smart decisions.

Impact On Home Ownership

A home equity loan uses your house as security. Missing payments can threaten your ownership. The loan amount depends on your home’s value. If property values drop, borrowing limits shrink. This can affect your plans and finances.

A mortgage is also tied to your home. It usually covers the full purchase price. Failing to pay a mortgage can lead to losing your home. The risk is higher because the loan is bigger. Your home is at stake until you finish payments.

Default And Foreclosure Risks

Default means missing loan payments. Both loans can lead to default if you struggle to pay. Default increases the chance of foreclosure. Foreclosure means the lender can sell your home. This helps them get back their money.

Home equity loans often have shorter terms. This can make monthly payments higher. Higher payments raise the chance of default. Mortgages tend to have longer terms and smaller payments. This can lower default risk but not eliminate it.

Use Cases And Scenarios

Choosing between a home equity loan and a mortgage depends on your financial needs and goals. Each option fits different situations. Knowing when to pick one can save money and stress.

Both loans use your home as security. But they serve different purposes. Understanding common use cases helps you decide wisely.

When To Choose A Home Equity Loan

Home equity loans suit one-time expenses. Examples include home repairs, medical bills, or debt consolidation.

The loan gives a fixed amount with fixed payments. This helps with budgeting and planning.

It works well if you have enough equity in your home. Also, if you want a lower interest rate than credit cards or personal loans.

Use a home equity loan for projects that add value to your home. Like remodeling a kitchen or adding a bathroom.

When A Mortgage Makes More Sense

Mortgages work best for buying a home or refinancing an existing loan. They usually cover larger amounts than home equity loans.

New mortgages may offer lower interest rates and longer repayment terms.

Choose a mortgage if you need to borrow a big sum over many years. This keeps monthly payments lower.

Refinancing a mortgage can lower your interest rate or monthly payment. It helps if your credit has improved or rates have dropped.

Credit: www.citizensbank.com

Tax Implications

Understanding tax implications is important when choosing between a home equity loan and a mortgage. Taxes affect how much you pay over time. Knowing the rules helps you make smart financial choices.

Deductibility Of Interest

Interest on a mortgage is usually tax deductible. This reduces your taxable income. You save money on your tax bill. Home equity loan interest can be deductible too. But only if you use the loan to buy, build, or improve your home.

Using a home equity loan for other purposes, like paying debts, often means no tax deduction. Keep good records of how you use the loan money. This helps when you file taxes.

Changes In Tax Laws

Tax laws about home loans change often. Recent rules limit the amount of mortgage debt you can deduct interest on. These changes affect both mortgages and home equity loans.

Staying updated on tax laws helps you plan better. Consult a tax expert for your specific situation. This ensures you follow current rules and get the best benefits.

Application And Approval

Applying for a home equity loan or a mortgage requires careful steps. The process and approval rules differ between these two loans. Knowing these differences helps you prepare better. This section explains the key points about application and approval.

Qualification Criteria

Home equity loans need you to have equity in your house. Lenders check your home’s value and your current mortgage balance. Your credit score and income also matter. Mortgage loans require proof of steady income and good credit. The lender looks at your debt and how much you can pay monthly. Both loans require documents like pay stubs and tax returns. But home equity loans focus more on your home’s equity. Mortgages focus more on your overall financial health.

Processing Timeframes

Home equity loans usually process faster. They often take a few weeks to approve. This is because the lender only checks your home value and finances. Mortgages take longer. They can take 30 to 60 days or more. This is due to more paperwork and detailed checks. Both loans need an appraisal of your home. Delays can happen if documents are missing or unclear. Being ready with all papers helps speed up both processes.

Expert Tips

Choosing between a home equity loan and a mortgage can be tricky. Experts suggest careful steps to help make the best choice. Understanding your money situation and getting good terms are key. These tips help you see which option fits your needs best.

Evaluating Your Financial Situation

Check your income and monthly expenses first. Know how much you can pay each month without stress. Think about your credit score; it affects loan approval and rates. Calculate the total cost of both options over time. Consider how long you plan to keep your home. These factors help decide which loan suits you.

Negotiating Better Terms

Talk to lenders about lowering interest rates. Ask about fees and if they can be waived. See if flexible payment plans are available. Compare offers from several lenders before choosing. A better deal can save you a lot of money. Don’t be afraid to ask questions and negotiate hard.

Frequently Asked Questions

What Is The Main Difference Between Home Equity Loan And Mortgage?

A home equity loan uses your home’s equity as collateral. A mortgage is a loan to buy a home. Equity loans are typically second loans, while mortgages are primary loans for home purchase.

Which Loan Has Lower Interest Rates: Home Equity Or Mortgage?

Mortgages generally have lower interest rates than home equity loans. Mortgage rates depend on the loan term and market conditions. Home equity loans often have higher rates due to increased risk for lenders.

Can I Use A Home Equity Loan To Buy A House?

No, home equity loans cannot be used to buy a house. They are loans against the equity of a home you already own. Mortgages are the proper loans for purchasing real estate.

Is A Home Equity Loan Or Mortgage Better For Debt Consolidation?

Home equity loans often have lower interest rates than credit cards, making them good for debt consolidation. Mortgages are not typically used for this purpose. Consider your financial situation before deciding.

Conclusion

Choosing between a home equity loan and a mortgage depends on your needs. Home equity loans offer fixed rates and set payments. Mortgages may have lower rates but vary with terms. Think about how much money you need and how long you want to pay it back.

Also, consider your credit score and financial situation. Both have pros and cons. Study them carefully before deciding. Make sure your choice fits your budget and goals. The right loan helps you manage money wisely. Take time to review all options first.