Are you thinking about remortgaging your home but wondering how equity release fits into the picture? Understanding how equity release works when you remortgage can unlock new financial opportunities and give you more control over your money.

Whether you want to free up cash for home improvements, help family members, or simply boost your savings, knowing the steps and benefits can make a big difference. Keep reading to discover how you can use equity release smartly during remortgaging—and make the most of your home’s value.

Credit: www.sunlife.co.uk

Basics Of Equity Release

Equity release lets homeowners access money tied up in their property. It works by turning part of your home’s value into cash. This cash can be used for various needs, such as home improvements or debt repayment. The loan or plan is repaid later, often when you sell your home or pass away.

Understanding the basics helps you see how equity release fits with remortgaging. It differs from traditional mortgages but can work alongside them. Knowing the key types, who qualifies, and the pros and cons is important before deciding.

Types Of Equity Release

There are two main types of equity release. The first is a lifetime mortgage. You borrow money secured against your home. You keep living there and pay no monthly fees. Interest builds up and is paid when you move or die.

The second type is home reversion. You sell part or all of your home to a company. You get cash or a lump sum. You still live in your home rent-free or pay a small rent.

Eligibility Criteria

To qualify for equity release, you must be at least 55 years old. Your home must be your main residence. Lenders usually require the property to be in good condition. The home must meet certain value limits. You should not have large outstanding mortgages or loans.

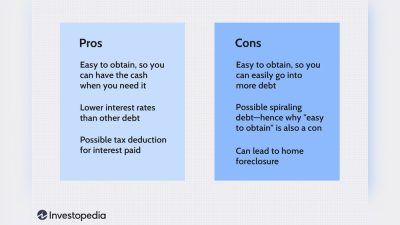

Benefits And Risks

Equity release offers cash without moving out. It helps with home repairs, debts, or daily expenses. No monthly repayments ease financial pressure.

Risks include reduced inheritance for heirs. Interest can grow and increase what you owe. Early repayment charges may apply. Not all schemes suit every homeowner. Careful planning is essential.

Remortgaging Explained

Remortgaging means switching your current mortgage to a new deal. You borrow money against your home again, but with different terms. This can help you save money or release some equity from your property.

Equity release lets you access some of your home’s value without selling it. When you remortgage, you can add equity release to your new mortgage deal. This means you get cash upfront by increasing your mortgage balance.

When To Remortgage

Remortgage when your current deal ends or interest rates drop. You might want to lower monthly payments or release equity for other needs. It can help if your home value has increased since you bought it.

Consider remortgaging if you want better mortgage terms. This could be a lower rate or a fixed rate for more stability. Timing is key to avoid high fees or penalties.

Types Of Remortgage Deals

Fixed-rate deals keep your interest the same for a set time. This gives you steady payments. Variable-rate deals change with the market, so payments may go up or down.

Some deals include equity release options. These let you borrow more than your current mortgage balance. You get extra cash but increase your debt.

Costs Involved

Remortgaging has fees like arrangement and valuation charges. You might pay early repayment fees on your old mortgage. Legal fees can apply for the new deal.

Equity release adds to your mortgage balance, so you pay more interest. Always check total costs before deciding. Plan carefully to avoid surprises.

Combining Equity Release With Remortgaging

Combining equity release with remortgaging can help homeowners access money while adjusting their mortgage terms. This option lets you take equity from your home and change your mortgage deal at the same time. It can support financial needs like home improvements or paying off debts. Understanding how these two work together is key to making smart choices.

How Equity Release Affects Remortgaging

Equity release reduces the home’s value available for remortgaging. The amount released adds to the mortgage debt. This can limit the new mortgage size. Lenders may see higher risk with equity release involved. Interest rates might be higher or offers stricter. This affects how much money you can borrow next.

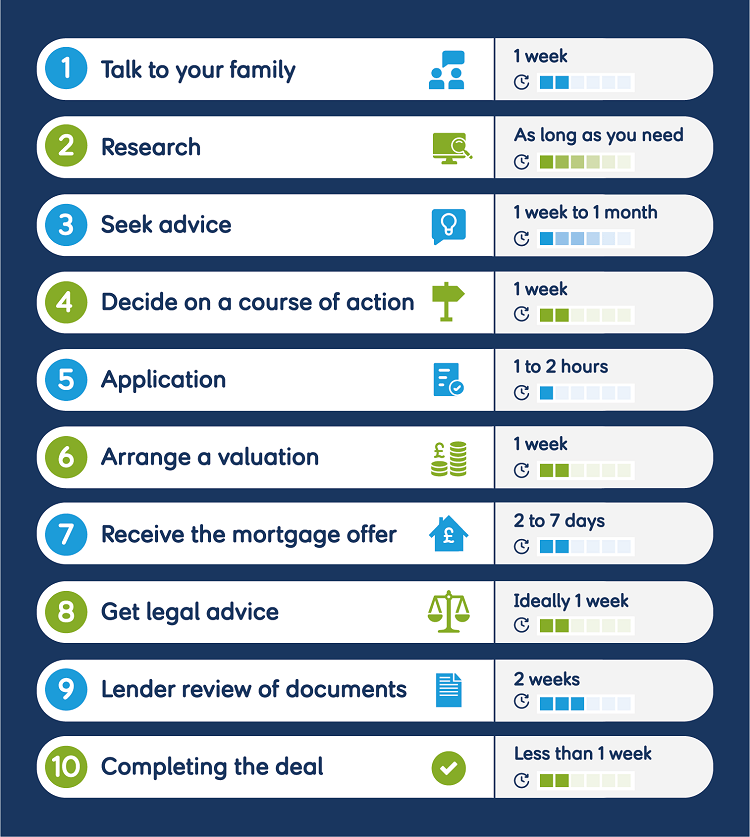

Process Steps

First, get a valuation of your home. Next, decide how much equity to release. Then, check your current mortgage terms for any fees. Apply for a new mortgage that includes released equity. The lender will review your finances and property. Once approved, the new mortgage pays off the old one and adds released funds. Finally, complete legal paperwork to finish the process.

Lender Requirements

Lenders require clear proof of income and expenses. They want to see you can repay the higher debt. Some lenders limit equity release with remortgages. Your home must meet certain conditions and valuations. You may need a solicitor to handle legal checks. Lenders expect full disclosure of any existing equity release deals.

Financial Implications

Understanding the financial implications of equity release during remortgaging is crucial. It affects your property value, monthly payments, and taxes. These factors influence your long-term financial health and decision-making.

Impact On Property Value

Equity release reduces the amount of ownership in your home. The lender holds a claim on part of your property’s value. This means your estate’s value decreases over time. It can affect what you leave to your heirs. Property value changes may impact future borrowing power too.

Effect On Monthly Payments

Equity release often means higher monthly payments. This happens because you borrow more money against your home. The interest can build up quickly if payments are low. Some plans allow interest to roll up, increasing the total debt. Careful budgeting helps manage these changes effectively.

Tax Considerations

Equity release usually does not create extra tax bills. The money borrowed is not treated as income. It is important to check if the interest is tax-deductible. Tax rules vary by location and personal situation. Consulting a tax advisor can clarify your specific case.

Common Challenges

Equity release can be helpful but brings some challenges during remortgaging. These issues may slow down the process or affect costs. Knowing common challenges helps prepare better. Here are key points to watch out for.

Approval Difficulties

Lenders may be cautious with equity release cases. They check the property value and borrower’s age carefully. Some lenders refuse remortgaging if equity release is involved. Approval takes longer than usual. This delay can cause stress and uncertainty.

Interest Rate Changes

Interest rates on equity release loans can rise over time. This increase affects the total amount owed. Remortgaging might come with higher rates than the original loan. Higher rates raise monthly payments or total costs. It is important to compare rates before deciding.

Contractual Restrictions

Equity release agreements often include strict rules. Some contracts limit the ability to remortgage early. Early repayment fees may apply, adding extra cost. Restrictions can reduce flexibility in managing your loan. Reading all contract terms is essential before signing.

Credit: sovereignboss.co.uk

Tips For A Smooth Process

Equity release can be complex, especially when remortgaging. A smooth process helps avoid delays and extra costs. Follow key tips to make your journey easier and clearer.

Choosing The Right Lender

Pick a lender experienced in equity release remortgages. Check their fees and terms carefully. Compare different offers to find the best fit. A good lender explains the process clearly and answers your questions.

Seeking Professional Advice

Talk to a financial advisor or mortgage broker. They understand equity release rules and options. Experts help you avoid mistakes and find the right plan. Their advice saves time and stress during remortgaging.

Timing Your Remortgage

Plan the timing based on your current mortgage deal. Start early to avoid penalties or extra charges. Allow time for lender approval and paperwork. Proper timing keeps your finances stable throughout the process.

Credit: everyinvestor.co.uk

Frequently Asked Questions

What Is Equity Release In Remortgaging?

Equity release lets homeowners access home value as cash. When remortgaging, it means increasing your mortgage to unlock equity. This cash can support expenses or debt. It’s crucial to compare deals and understand fees before proceeding.

Can I Combine Equity Release With A Remortgage?

Yes, you can combine equity release with remortgaging. This means refinancing your mortgage to release some home equity. It often requires lender approval and impacts monthly payments. Always assess affordability and long-term costs before combining these options.

How Does Remortgaging Affect Equity Release Terms?

Remortgaging can change your equity release terms by adjusting interest rates or loan amounts. It might affect your repayment schedule and fees. Review all new terms carefully to ensure they align with your financial goals and don’t increase risks.

Are There Risks With Equity Release During Remortgaging?

Yes, risks include increased debt, reduced inheritance, and higher interest costs. Remortgaging with equity release can complicate finances and affect future borrowing. Seek professional advice to fully understand these risks before proceeding.

Conclusion

Equity release can affect your remortgaging options and costs. Understanding how it works helps you make smart choices. Check the terms carefully before deciding. Talk to a mortgage advisor for clear advice. Remember, your home’s value and loan size matter a lot.

Take time to compare deals and find the best fit. Planning ahead makes the process easier and less stressful. Keep your financial goals in mind at every step. This way, you stay in control of your money and home.