Are you looking to unlock some cash from your home without going through the hassle of remortgaging? You might think releasing equity means you have to switch your mortgage, but that’s not always the case.

Imagine getting extra funds for home improvements, debt consolidation, or even a dream vacation—without the stress of a full mortgage change. You’ll discover practical ways to release equity while keeping your current mortgage intact. Keep reading to find out how you can make your home work harder for you, with less hassle than you might expect.

Equity Release Basics

Equity release basics help homeowners understand their options. It explains how to access money tied up in a home. Many people want to release equity without remortgaging. This means getting cash without changing their mortgage lender or terms.

Knowing the fundamentals can guide better financial choices. It also clears up common questions about equity release methods.

What Is Home Equity

Home equity is the part of your house you fully own. It is the current value of your home minus any debts on it. For example, if your home is worth $200,000 and you owe $100,000, your equity is $100,000.

Equity grows as you pay down your mortgage or if property values rise. You can use equity as a financial resource for many needs.

Common Equity Release Methods

Several ways exist to release equity without changing your mortgage. One method is a home equity loan. This loan uses your home as security but does not replace your mortgage.

Another option is a home equity line of credit (HELOC). This works like a credit card with a limit based on your equity. You borrow what you need and repay with interest.

Some people choose a sale and leaseback. They sell part of their home and rent it back. This frees up cash while letting them stay in their home.

Each method suits different needs and situations. Understanding these options helps make smart financial decisions.

Remortgaging Vs Other Options

Many homeowners want to release equity without changing their mortgage. There are several options to consider besides remortgaging. Each choice affects your finances in different ways. Understanding these options helps you pick what fits best.

How Remortgaging Works

Remortgaging means replacing your current mortgage with a new one. The new mortgage often has different terms or interest rates. You can borrow more money by increasing the mortgage amount. This extra money is the equity you release.

The lender pays off your old mortgage first. Then, you start a new loan with fresh conditions. This process may involve fees and paperwork. The new mortgage may last for a longer or shorter period.

Drawbacks Of Remortgaging

Remortgaging can involve extra costs like legal fees and valuation charges. Some lenders charge penalties for leaving early. The process can take weeks to complete. It may affect your credit score temporarily.

Not all homeowners qualify for remortgaging. Your home value and income must meet lender rules. The new mortgage rate might be higher than before. These factors make remortgaging less attractive for some people.

Equity Release Without Remortgaging

Equity release does not always mean remortgaging your home. Some options let you access your home’s value without changing your main mortgage. These methods can provide cash while keeping your current loan intact.

Understanding these alternatives helps you make better choices. Each option has unique features and suits different needs.

Home Equity Loans

Home equity loans give a lump sum of money. You borrow against the value of your home. The loan has a fixed interest rate and fixed payments. It works like a second mortgage but does not replace your main loan. You repay it over time.

Home Equity Lines Of Credit (helocs)

HELOCs act like a credit card tied to your home’s value. You can borrow money as needed, up to a limit. Interest rates are usually variable. You pay interest only on the amount you use. It offers flexibility for ongoing expenses.

Sale And Leaseback

Sale and leaseback lets you sell your home to an investor. Then, you rent the same property from them. This way, you get cash from the sale. You keep living in your home but as a tenant now. It can be a good option for some homeowners.

Shared Equity Schemes

Shared equity schemes involve selling part of your home’s value. A company or government shares ownership with you. You get cash without borrowing money. When you sell, you share the profit or loss with the partner. It reduces financial risk but also future gains.

Credit: ukmoneyman.com

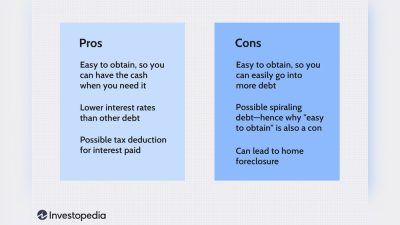

Pros And Cons Of Each Method

Releasing equity from your home can be done in different ways. Each method has its own benefits and drawbacks. Understanding these helps you choose the best option for your needs. This section compares the pros and cons of releasing equity without remortgaging and other common methods.

Cost Implications

Releasing equity without remortgaging often has lower upfront fees. It may avoid some legal and valuation costs. But interest rates can be higher than a new mortgage deal. Remortgaging might have higher setup fees but usually offers lower interest rates. Monthly repayments could be less with remortgaging. Consider all fees, including early repayment charges on your current mortgage.

Risk Factors

Keeping your current mortgage means less paperwork and risk of rejection. Yet, higher interest rates can increase your monthly costs. Not remortgaging may limit how much equity you can release. Remortgaging can reset your mortgage term, affecting long-term payments. Both methods carry the risk of rising interest rates. Evaluate your financial stability before deciding.

Flexibility

Releasing equity without remortgaging often allows quicker access to funds. It may suit short-term financial needs better. Remortgaging can provide a larger lump sum but takes longer to arrange. Some remortgage deals offer flexible repayment options. Without remortgaging, you might face limits on extra payments or early repayment. Choose the option that fits your lifestyle and plans.

Eligibility And Qualification

Releasing equity without remortgaging can be a simple option for some homeowners. Understanding eligibility and qualification is key. Lenders check a few main factors before approving your request. These help them decide if you can borrow extra money without changing your mortgage.

Credit Requirements

Lenders look closely at your credit score. A good score shows you pay debts on time. Scores above 650 usually have better chances. Low scores might mean higher interest or denial. Some lenders want proof of steady income too. This shows you can repay the borrowed money. Missing payments or high debt can hurt your chances.

Property Value Considerations

The value of your home matters a lot. Lenders use recent appraisals to check this. A higher value means more equity available. Most lenders allow borrowing up to 85% of your home’s worth. If the value drops, you may qualify for less. The property’s condition also matters. Well-maintained homes get better offers.

Credit: www.youtube.com

Impact On Financial Health

Releasing equity without remortgaging affects your financial health in many ways. It changes how much money you owe and your future financial plans. Understanding these effects helps you make smart decisions. Careful thought is important before choosing this option.

Effect On Credit Score

Releasing equity without remortgaging can impact your credit score. Lenders may check your credit more often. This can cause a small drop in your score. Borrowing more money increases your total debt. Higher debt can lower your credit rating.

Paying back on time helps keep your credit healthy. Missing payments harms your score quickly. Managing new debt carefully is key to avoid problems.

Long-term Financial Planning

This option changes your future money plans. You may have extra cash now, but debt stays longer. This affects your ability to save or invest. Monthly payments might increase, reducing your budget.

Think about your income and expenses over time. Plan how you will repay the borrowed amount. Avoid taking more debt than you can handle. Proper planning keeps your finances stable and secure.

Tips For Choosing The Right Option

Choosing the right way to release equity without remortgaging needs careful thought. The choice affects your money and future plans. Understanding your options helps you avoid risks and make smart decisions.

Consider what matters most for your finances. Seek advice from experts who know the market. These steps can guide you to the best option for your situation.

Assessing Your Financial Goals

Start by listing your financial needs. Do you want cash for home repairs, debt, or another purpose? Think about how long you plan to keep your home. Know your comfort level with monthly payments or interest rates. This clarity helps narrow down suitable choices.

Calculate how much money you need now. Avoid borrowing more than necessary. Also, consider how releasing equity affects your future savings or pension plans. Clear goals lead to better decisions.

Consulting Financial Advisors

Talk to a financial advisor who understands equity release options. They explain complex terms simply. Advisors check your situation and offer tailored advice. They also highlight risks you might miss.

Choose someone independent and trustworthy. Verify their credentials before sharing personal details. Good advice saves money and stress later. Don’t hesitate to ask questions or request examples.

Credit: ukmoneyman.com

Frequently Asked Questions

Can You Release Equity Without Remortgaging?

Yes, you can release equity without remortgaging through a secured loan or a homeowner’s loan. These options let you access cash without changing your current mortgage terms.

What Are Alternatives To Remortgaging For Equity Release?

Alternatives include secured loans, personal loans, or a home equity line of credit (HELOC). These don’t require changing your mortgage but may have higher interest rates.

Is Equity Release Without Remortgaging More Expensive?

It can be more costly due to higher interest rates and fees. Always compare total costs before choosing this option.

How Does A Secured Loan Help Release Equity?

A secured loan uses your property as collateral, letting you borrow money against its value without remortgaging your home.

Conclusion

Releasing equity without remortgaging is possible in some cases. You can use options like a second charge loan or a home equity loan. These choices may save time and reduce paperwork. Still, each method has risks and costs to consider.

Always check your financial situation carefully before deciding. Talk to a trusted advisor to find the best way for you. Understanding your options helps you make smart money choices. Equity release doesn’t always mean changing your mortgage.