Thinking about tapping into your home’s value with a home equity loan? It sounds like a smart way to get cash for big expenses, like renovations or debt consolidation.

But before you dive in, it’s important to understand both the benefits and the risks. What if this loan helps you save money, or what if it puts your home in danger? You’ll discover the key pros and cons of taking a home equity loan, so you can make the best decision for your financial future.

Keep reading to find out what you need to know before you borrow.

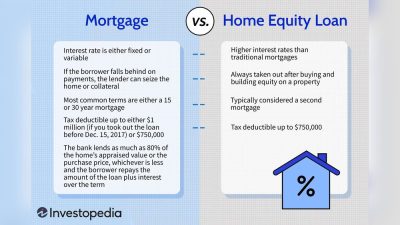

What Is A Home Equity Loan

A home equity loan lets you borrow money using your home’s value. It is a type of loan where your house acts as collateral. This means the lender can take your home if you don’t repay the loan.

Home equity loans usually have fixed interest rates. You receive the loan amount in one lump sum. Then, you pay back the loan in regular monthly payments over time.

How Does A Home Equity Loan Work?

You borrow money based on your home’s equity. Equity is the difference between your home’s value and what you owe. For example, if your home is worth $200,000 and you owe $150,000, your equity is $50,000.

The lender decides how much you can borrow. This amount depends on your equity and credit score. The loan is paid back in fixed monthly payments.

Types Of Home Equity Loans

There are two main types of home equity loans. The first is a lump-sum loan with fixed interest. You get all the money at once. The second is a home equity line of credit (HELOC). This works like a credit card with a limit you can borrow from anytime.

Uses Of A Home Equity Loan

Homeowners use these loans for many reasons. Common uses include home repairs, paying off debt, and covering education costs. Some use the money for medical bills or emergencies. The loan provides access to large sums at lower interest rates than credit cards.

Credit: www.experian.com

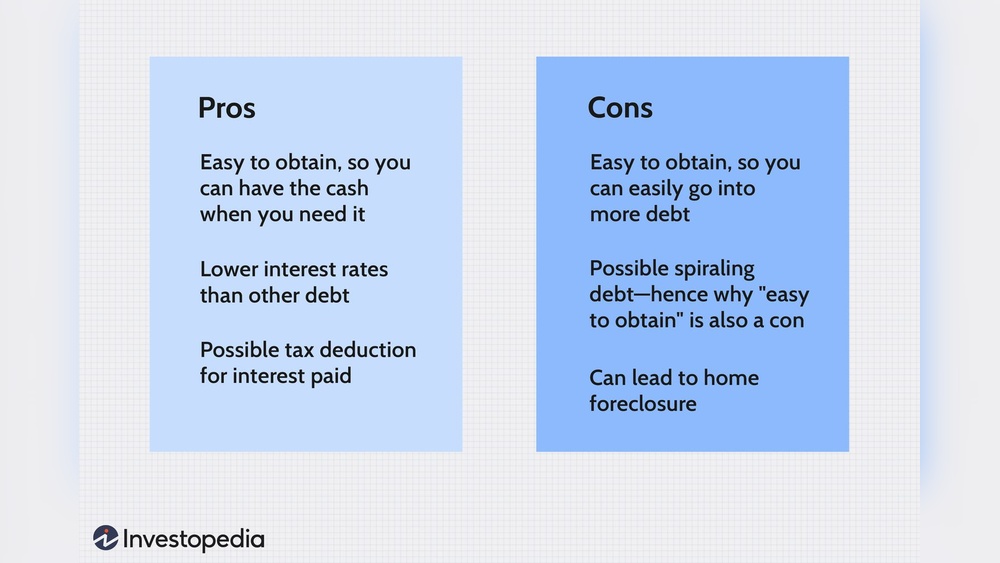

Benefits Of Home Equity Loans

Home equity loans offer several benefits that many homeowners find useful. They provide a way to use the value of your home for cash. This cash can help with big expenses or debt.

Understanding these benefits helps you decide if a home equity loan fits your needs.

Lower Interest Rates

Home equity loans often have lower interest rates than credit cards or personal loans. This makes borrowing cheaper. Lower rates mean you pay less money over time. It is easier to manage monthly payments too.

Tax Advantages

Interest on home equity loans may be tax-deductible. This depends on how you use the loan. Using the money for home improvements usually qualifies. Tax savings reduce the overall cost of the loan.

Lump Sum Access

These loans give you a lump sum of money at once. This is helpful for large expenses like home repairs or education. You know the total amount and repayment plan upfront. It helps with budgeting and planning.

Flexible Use Of Funds

You can use the loan money for many purposes. Pay off high-interest debt, fund medical bills, or make home upgrades. There are fewer rules on spending compared to other loans. This flexibility makes home equity loans popular.

Drawbacks Of Home Equity Loans

Home equity loans can offer cash using your home’s value. They seem helpful but carry some risks. Knowing the drawbacks helps make a smart choice. These loans affect your finances in many ways. Here are key problems to watch out for.

Risk Of Foreclosure

Your home serves as loan security. Missed payments can lead to losing your home. Foreclosure means the bank can sell your house. This risk makes the loan serious and risky. Protect your home by paying on time.

Closing Costs And Fees

Home equity loans often have upfront costs. These include appraisal, application, and processing fees. These fees add to your loan total. Sometimes, fees can be hundreds or thousands of dollars. Factor these costs before borrowing.

Impact On Credit Score

Taking a home equity loan affects your credit. Applying for the loan results in a hard credit check. This can lower your credit score slightly. Also, missing payments damages credit history. Good credit means better loan options.

Potential For Overborrowing

Easy access to cash can lead to borrowing too much. Overborrowing creates heavy monthly payments. It can strain your budget and cause stress. Borrow only what you need and can repay. Keep control over your finances.

Credit: www.ussfcu.org

When To Consider A Home Equity Loan

A home equity loan can be a useful tool for managing your finances. It lets you borrow money using your home’s value. This loan works best in certain situations. Knowing when to consider a home equity loan helps you make smart choices.

Use it for expenses that add value or reduce high-interest debt. Avoid using it for daily expenses or things that do not last long.

Home Improvement Projects

Home equity loans are ideal for home repairs and upgrades. Use the loan to fix your roof, update your kitchen, or add a new room. These projects increase your home’s value. This makes the loan a good investment.

Debt Consolidation

Consolidate high-interest debts like credit cards with a home equity loan. This loan usually has a lower interest rate. It helps you save money on interest. It also simplifies payments by combining debts into one.

Emergency Expenses

Emergency costs such as medical bills or urgent repairs can be covered. A home equity loan offers a larger sum than credit cards or personal loans. It can provide peace of mind during tough times. Use it carefully to avoid future financial strain.

Alternatives To Home Equity Loans

Home equity loans are popular, but not the only choice for borrowing money. Several alternatives offer different benefits and risks. Knowing these options helps you decide what fits your needs best.

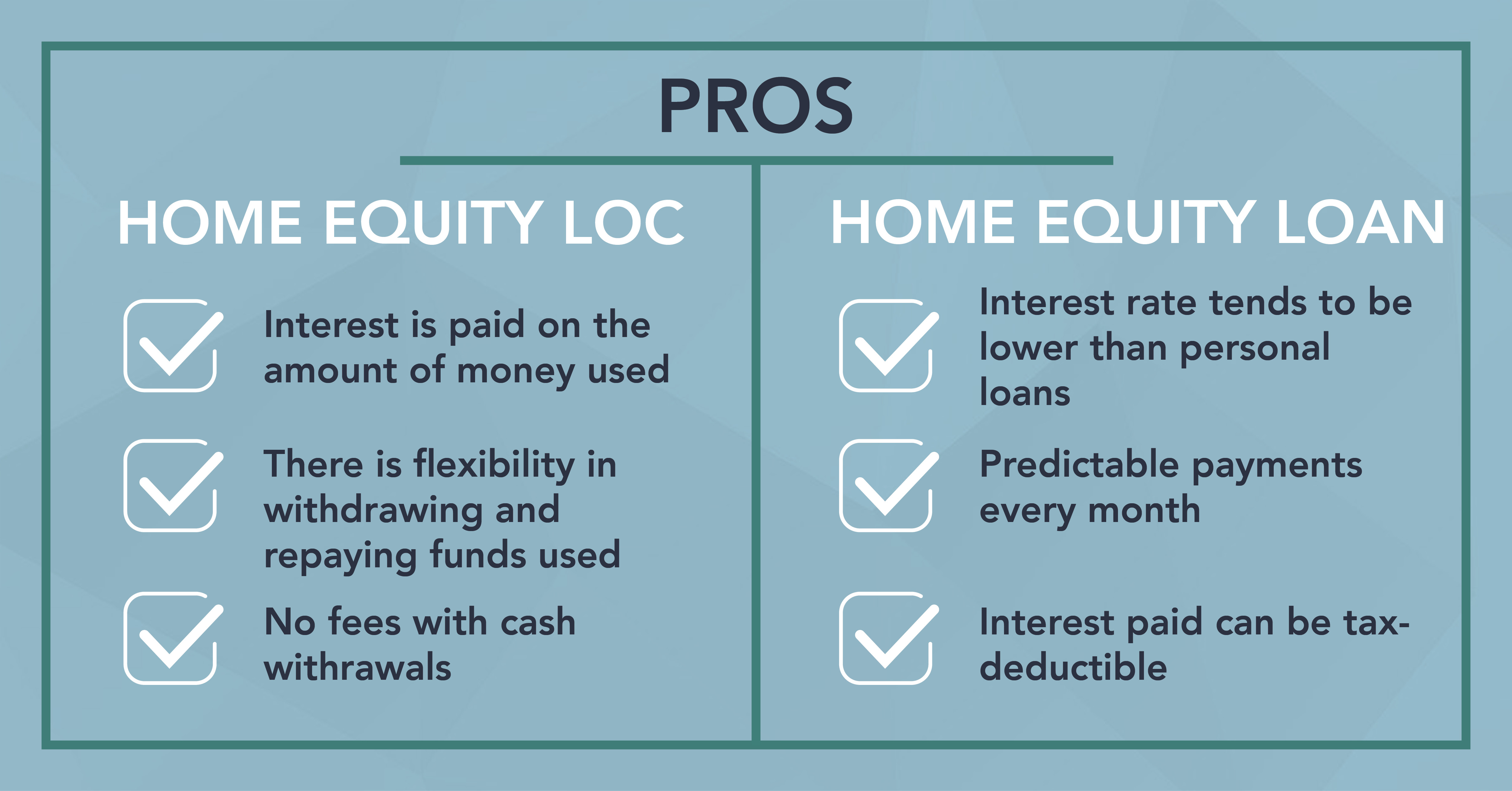

Home Equity Line Of Credit (heloc)

A HELOC works like a credit card with your home as collateral. You get a credit limit based on your home’s value. You borrow money as needed and pay interest only on what you use. This option offers flexibility and lower initial costs. Interest rates may change over time. It suits those who want ongoing access to funds.

Personal Loans

Personal loans do not require your home as security. You get a fixed amount of money with a set repayment plan. These loans usually have higher interest rates than home equity loans. Approval depends on your credit score and income. They are faster to get and less risky for your home.

Refinancing

Refinancing replaces your current mortgage with a new one. It can lower your interest rate or change your loan term. You can borrow extra money during refinancing, called a cash-out refinance. This option may reduce monthly payments or raise available cash. Closing costs can be higher than other loans.

Credit: waldostate.bank

Tips For Applying

Applying for a home equity loan needs careful thought. It can affect your finances for years. Follow some simple tips to make the process easier and safer. These tips help you choose well and avoid common mistakes.

Evaluate Your Financial Situation

Check your income and expenses first. Know how much you can repay each month. Think about your job stability and future costs. Avoid borrowing more than you can handle. A clear budget helps prevent financial stress.

Compare Lenders

Look at different lenders’ offers. Compare interest rates and fees carefully. Some lenders may have hidden costs. Ask about early repayment penalties. Choose the lender with the best overall deal.

Understand Terms And Conditions

Read all loan documents thoroughly. Know the loan length and payment schedule. Understand what happens if you miss payments. Learn about any changes in interest rates. Clear knowledge avoids surprises later.

Frequently Asked Questions

What Is A Home Equity Loan And How Does It Work?

A home equity loan lets you borrow against your home’s value. It provides a lump sum with fixed interest and repayment terms. You repay it monthly, using your home as collateral. This loan is ideal for large, one-time expenses or debt consolidation.

What Are The Main Advantages Of Home Equity Loans?

Home equity loans offer lower interest rates compared to credit cards. They provide fixed monthly payments and predictable costs. Borrowers can access large funds for home improvements or major expenses. Interest may be tax-deductible, making them cost-effective for eligible homeowners.

What Risks Should I Consider Before Getting A Home Equity Loan?

Home equity loans put your home at risk if you can’t repay. Missing payments can lead to foreclosure. They increase your overall debt and reduce home equity. Also, closing costs and fees may apply, making it important to assess your financial stability first.

How Do Home Equity Loans Compare To Home Equity Lines Of Credit?

Home equity loans provide a lump sum with fixed payments. HELOCs work like credit cards, allowing flexible borrowing and variable rates. Loans suit one-time expenses, while HELOCs fit ongoing or unpredictable costs. Both use your home as collateral and require careful financial planning.

Conclusion

Taking a home equity loan has clear benefits and some risks. It offers easy access to cash for big expenses. You can get lower interest rates than with other loans. But, you must repay on time to avoid losing your home.

Your home’s value and your credit score affect loan terms. Think carefully about your financial situation before applying. This loan suits some people but not everyone. Weigh the pros and cons to make a smart choice. Your home is valuable; protect it wisely.