Are you curious about how to unlock the value tied up in your home without having to sell it? Understanding what equity release is in the UK could be the key to your financial freedom.

Whether you want extra cash for home improvements, travel, or simply to boost your income, equity release might be the solution you didn’t know you needed. This article will guide you through everything you need to know, helping you make confident decisions about your money and your future.

Keep reading to discover how equity release works and if it’s the right choice for you.

Equity Release Basics

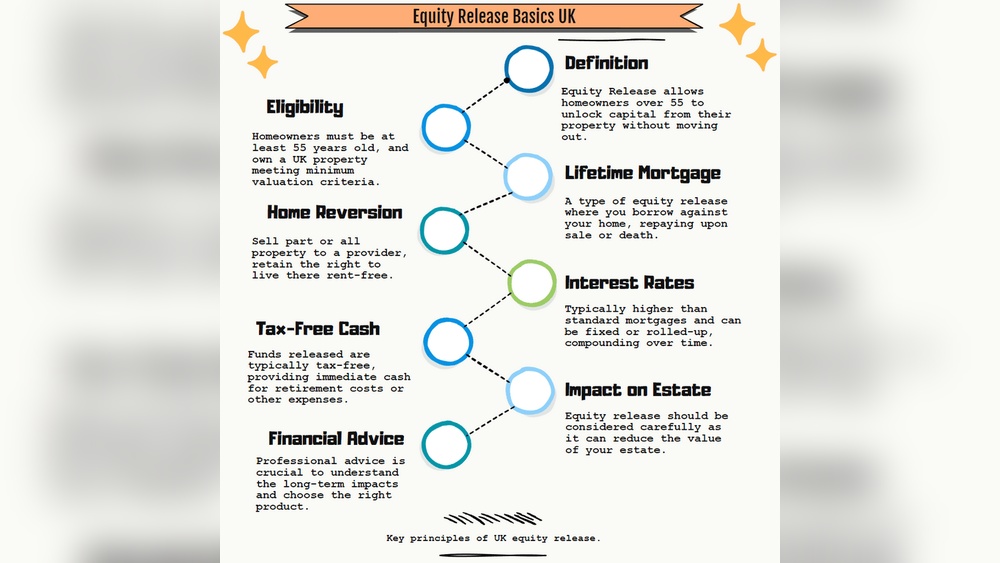

Equity release lets homeowners access money tied up in their property. It is popular among older people in the UK. This money can support retirement or pay for home changes. It works without selling the house immediately. Instead, the loan is paid back later, usually when the homeowner dies or moves out.

This section explains the basics of equity release. Understanding the types and who can qualify helps make smart choices.

Types Of Equity Release

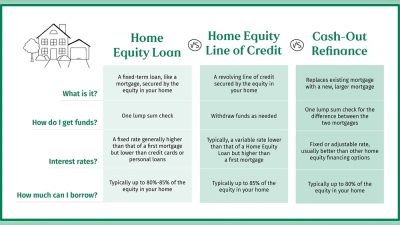

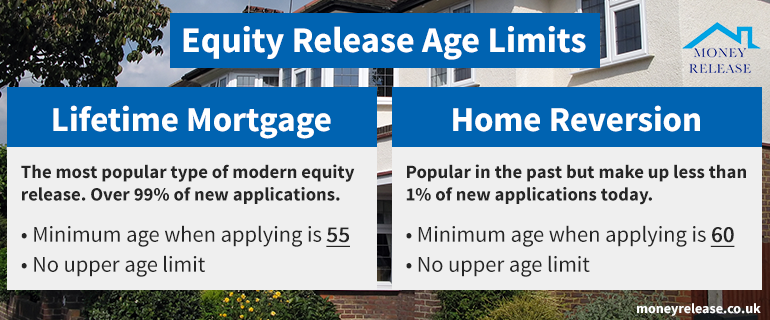

Two main types exist: lifetime mortgages and home reversion plans. Lifetime mortgages let you borrow money against your home. You keep full ownership of your house. Interest builds up over time and is paid later. Home reversion plans sell part or all of your home. You get a lump sum or regular payments. You still live in your home rent-free. The buyer owns the part of the home they bought.

Who Can Qualify

Usually, you must be 55 or older to qualify. You need to own your home or have a large share of it. The home must meet certain conditions, like being your main residence. Lenders check if you understand the deal. They also assess the value of your property. Health and financial status may affect eligibility. Some products suit specific needs better than others.

How Equity Release Works

Equity release lets homeowners get cash from their property’s value. It works by using your home as security for a loan. You can access money without selling your house or moving out.

There are different ways to take the money. You can take it all at once or in smaller amounts over time. The loan grows with interest and is paid back later, usually after you pass away or move into care.

Lump Sum Vs. Drawdown

A lump sum means you get one big payment. You receive all the money at once. Good for big expenses like home repairs or paying off debts.

Drawdown lets you take money bit by bit. You only borrow what you need. Interest is charged only on the amount used. It gives more control over the loan.

Interest And Repayment

Interest builds up on the loan over time. It adds to the total amount you owe. You don’t usually make monthly payments.

The loan is repaid when you die or move to care. Your home is sold, and the lender gets their money. Any leftover money goes to your family or estate.

Benefits Of Equity Release

Equity release offers several benefits for homeowners aged 55 and over. It helps you use the value of your home without selling it. Many people find this option useful for extra money in retirement. Understanding these benefits can help you decide if equity release suits your needs.

Accessing Hidden Wealth

Your home holds value you may not see every day. Equity release lets you access this hidden wealth. You receive cash based on your home’s worth. This money can pay for home improvements, debts, or daily costs. It can improve your quality of life without moving house.

Flexibility And Freedom

Equity release offers flexible ways to get cash. You can take a lump sum or smaller amounts over time. This freedom helps you manage money better during retirement. Use funds for holidays, healthcare, or family support. No monthly repayments are needed; interest adds up over time.

Risks And Considerations

Equity release can help you access money from your home. It has benefits but also risks to think about. Understanding these risks helps you make a smart choice.

Equity release reduces the value of your home. This can affect what you leave for your family. Knowing the impact on inheritance is very important.

Impact On Inheritance

Equity release lowers the amount of money left to heirs. The loan and interest reduce your home’s value. Your family may get less money than expected.

Some plans add interest over time. This can make the debt grow quickly. Your home might be worth less than the debt when you pass away.

Planning carefully can protect your loved ones. Talk with family and a financial expert before deciding.

Effect On Benefits And Taxes

Equity release can change your benefits. Some benefits depend on your income and savings. Extra money from equity release might reduce or stop these benefits.

You usually do not pay income tax on the money taken out. But changes in your financial situation can affect tax rules. Getting advice helps you avoid surprises.

Check how equity release fits with your benefits and tax status. This avoids problems later.

Choosing The Right Plan

Choosing the right equity release plan matters a lot. It affects your finances and future. Each plan has different features and costs. Understanding these helps you pick the best option for your needs. Take time to explore your choices carefully.

Comparing Providers

Providers offer various equity release plans. Some have better interest rates or lower fees. Check what each provider includes in their plan. Look at customer reviews and ratings. See how long the company has been in business. Compare their reputations and support services. These points help you find a trustworthy provider.

Getting Professional Advice

Talking to an expert can clear doubts. Financial advisers explain complex terms simply. They show how plans affect your money and home. Advisers help you understand risks and benefits. They suggest plans that suit your situation. This advice protects you from poor choices. Always choose a qualified adviser registered with official bodies.

Credit: www.moneyrelease.co.uk

Legal And Regulatory Safeguards

Equity release in the UK is a serious financial decision. Legal and regulatory safeguards protect consumers throughout the process. These rules make sure that people understand the terms and are treated fairly. The safeguards also provide a safety net if anything goes wrong.

Consumer Protections

Consumers have strong protections when using equity release products. Providers must give clear, honest information before any agreement. This includes details about costs, risks, and how the loan affects your home. Customers have the right to cancel within 14 days. This cooling-off period helps people rethink their choice without pressure.

Equity release deals must also follow strict rules on affordability. This prevents people from borrowing more than they can manage. Independent advice is required, so customers get guidance from qualified experts. These protections work to keep people safe from poor decisions or scams.

Role Of The Financial Conduct Authority

The Financial Conduct Authority (FCA) regulates equity release providers. The FCA sets standards for fairness, transparency, and customer care. They monitor companies to ensure compliance with the rules. The FCA can take action against firms that break these rules.

The FCA requires providers to give clear information about products and risks. They also check that advice is suitable for each customer. This helps protect vulnerable people from bad deals. The FCA’s role builds trust in the equity release market and helps consumers feel secure.

Real-life Equity Release Examples

Real-life examples help explain how equity release works in the UK. They show how people use their home’s value for cash. Each story is different but clear. These examples make it easier to understand the benefits and risks.

Equity release can help with many needs. Some use it for home repairs, others for family support or travel. Seeing real cases gives a better view of its practical use.

Helping With Home Repairs And Improvements

John and Mary needed money to fix their old roof. They used equity release to get a lump sum. This helped them pay for repairs without a loan. Their home stayed safe, and they did not lose ownership.

Supporting Family Members

Sarah wanted to help her daughter buy a house. She chose equity release to give her a gift. This made it easier for her daughter to pay the deposit. Sarah still lives in her home and keeps control.

Enjoying Retirement And Travel

Tom and Linda used equity release to fund a holiday. They took out a small amount and planned a trip abroad. The money made their retirement more enjoyable. They did not need to move or sell their home.

Paying Off Debts

Emma had high credit card debts. She used equity release to clear her debts quickly. This lowered her monthly expenses and stress. She kept living in her home without extra bills.

Credit: www.youtube.com

Credit: everyinvestor.co.uk

Frequently Asked Questions

What Is Equity Release In The Uk?

Equity release in the UK lets homeowners access cash from their property. It’s mainly for people over 55. You keep living in your home while unlocking its value without selling it.

How Does Equity Release Work In The Uk?

You borrow money secured on your home’s value. The loan plus interest is repaid when you die or move out. There are two main types: lifetime mortgages and home reversion plans.

Who Can Apply For Equity Release In The Uk?

Typically, UK homeowners aged 55 or older qualify. Your property must meet lender criteria. It suits those needing extra income or funds for retirement expenses.

What Are The Risks Of Equity Release Uk?

Interest can build up quickly, reducing inheritance. Your home’s value might drop, affecting the loan amount. Always seek professional advice to understand all risks before proceeding.

Conclusion

Equity release helps older homeowners access money from their homes. It can provide extra cash without moving out. But it reduces the home’s value for heirs. Understanding the risks and benefits is very important. Speak with a trusted advisor to get clear advice.

Make sure it fits your needs and plans. This way, you can make a smart choice about your finances. Take your time and review all options carefully. Equity release is not for everyone, but it may help some.