Thinking about tapping into your home’s value with a home equity loan? Before you take the next step, it’s important to understand exactly how much this type of loan will cost you.

You want to avoid surprises that could strain your budget or slow down your plans. You’ll discover the key factors that affect the cost of a home equity loan and learn how to calculate what it might mean for your wallet.

Keep reading to make a smart, confident decision about using your home equity.

Home Equity Loan Basics

Understanding home equity loans helps you decide if this loan fits your needs. These loans use your home’s value as security. You borrow a lump sum of money and repay it over time. Interest rates often stay fixed, so monthly payments remain steady.

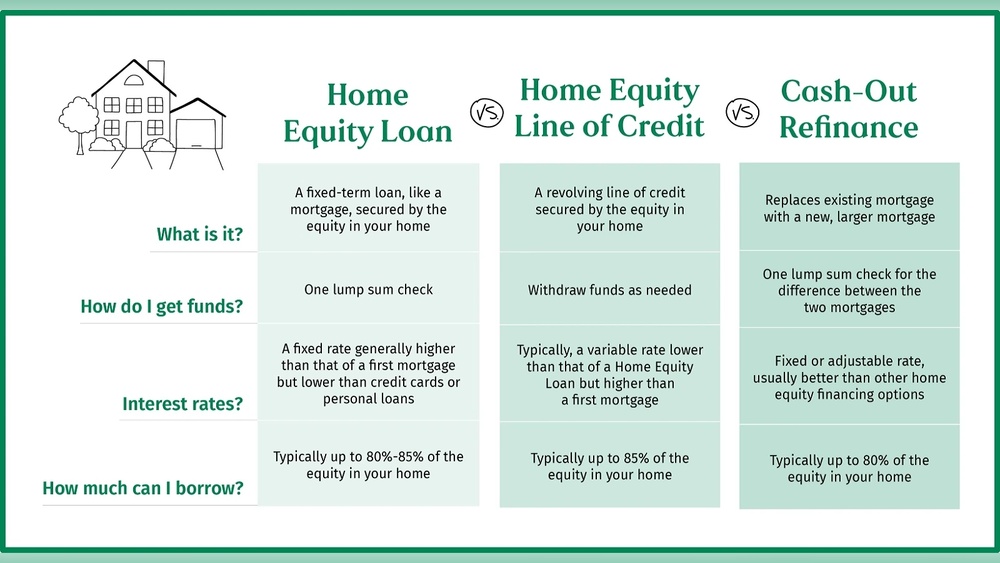

This type of loan differs from a home equity line of credit. It provides a set amount upfront instead of a credit limit to draw from. Knowing the basics clears confusion about costs and terms.

What Is A Home Equity Loan

A home equity loan is money borrowed against your home’s value. You repay it with interest over a set term. The loan amount depends on your home equity and lender rules. It usually has a fixed interest rate and fixed payments. This makes budgeting easier for many borrowers.

Common Uses For Home Equity Loans

Many use home equity loans for home repairs or improvements. These loans can also pay off high-interest debts. Some borrowers use them for education or major purchases. The funds often come with lower interest than credit cards. Planning the loan use helps avoid unnecessary debt.

Credit: www.esl.org

Core Costs Of Home Equity Loans

Understanding the core costs of home equity loans helps you plan your budget. These costs affect the total amount you repay. Knowing each cost lets you compare offers wisely.

Interest Rates Explained

Interest rates determine how much extra you pay on the loan. They are usually lower than credit cards but vary by lender. Fixed rates stay the same, while variable rates can change over time. A lower rate means lower monthly payments.

Loan Origination Fees

Loan origination fees cover the lender’s work to process your loan. This fee is often a percentage of the loan amount. It can add several hundred dollars to your cost. Some lenders may waive this fee, but many include it.

Appraisal Charges

The lender needs to know your home’s value before approving the loan. An appraisal is an inspection by a professional appraiser. This fee usually costs between $300 and $500. The appraisal helps set the maximum loan amount you can get.

Hidden Fees To Watch For

Home equity loans can seem simple, but they often come with hidden fees. These fees add to the total cost and affect your budget. Knowing about them helps avoid surprises.

Some fees are not clear at first. Lenders may not mention them upfront. Watch closely for these extra costs before signing any agreement.

Prepayment Penalties

Some lenders charge a fee if you pay off the loan early. This is called a prepayment penalty. It stops you from saving money by paying off your loan fast. Always ask if this fee applies before choosing a loan.

Closing Costs

Closing costs include many small fees for processing your loan. These may cover appraisal, title search, and paperwork. Closing costs can be hundreds or thousands of dollars. Check the estimated closing costs so you can plan ahead.

Annual Or Maintenance Fees

Some loans have yearly fees just for keeping the account open. These annual or maintenance fees add to your expenses. Even if you do not use the loan much, these fees still apply. Confirm if your loan has these charges to avoid surprises.

Credit: www.experian.com

Additional Expenses Impacting Cost

Home equity loans come with more costs than just interest rates. These additional expenses can add up quickly. Knowing these fees helps you plan your budget better. Below are some common extra costs you should expect.

Title Search And Insurance

A title search checks if your home has any legal issues. This process makes sure the lender can claim the property if needed. Title insurance protects you and the lender from future problems. These fees usually range from $200 to $500. They vary by location and property value.

Credit Report Fees

Lenders check your credit to decide your loan terms. This check requires a credit report fee. The cost is small, often between $20 and $50. It covers the lender’s cost to access your credit history. This fee is usually part of your loan closing costs.

Flood Certification Charges

Lenders must know if your home is in a flood zone. Flood certification determines this risk. If your property is in a flood-prone area, you may need flood insurance. The certification fee is typically $15 to $25. This small cost ensures the lender follows federal rules.

Factors That Influence Overall Expenses

Several factors affect the total cost of a home equity loan. Understanding these helps you plan better. Each factor changes how much you pay in interest and fees. Knowing them can save you money and avoid surprises.

Loan Amount And Term

The size of your loan affects the cost directly. Larger loans usually have higher interest charges. The loan term also matters. Longer terms mean lower monthly payments but more interest overall. Shorter terms cost less in interest but raise monthly payments.

Credit Score Effects

Your credit score influences your interest rate. Higher scores get better rates and lower costs. Lower scores may lead to higher rates and more fees. Lenders see credit scores as a risk measure. A good score can save you hundreds or thousands.

Lender Variations

Different lenders charge different fees and rates. Some have low fees but higher interest rates. Others offer promotions or flexible terms. Compare lenders to find the best deal. Pay attention to hidden fees like application or closing costs.

Credit: beehive.org

Strategies To Reduce Home Equity Loan Costs

Home equity loans can be costly. Knowing how to lower these costs helps save money. Small steps make a big difference. Use smart strategies to pay less on your loan.

Shop Around For Lenders

Different lenders offer different rates and fees. Check many lenders before choosing one. Compare interest rates, loan terms, and closing costs. This helps find the best deal for your budget.

Negotiate Fees

Fees like application, appraisal, and closing costs can add up. Ask lenders to lower or waive some fees. Negotiation can reduce your overall loan cost. It is worth trying, as lenders want your business.

Consider Alternatives

Other options may cost less than a home equity loan. Personal loans and refinancing might have lower fees. Choose the option that fits your financial needs best. Avoid paying extra when a cheaper choice exists.

Frequently Asked Questions

What Are The Typical Interest Rates For Home Equity Loans?

Home equity loan interest rates usually range from 3% to 8%. Rates depend on credit score, loan amount, and lender policies. Fixed rates are common, providing predictable monthly payments. Comparing multiple lenders helps find the best rate for your financial situation.

What Fees Are Associated With Home Equity Loans?

Home equity loans often include appraisal fees, origination fees, and closing costs. These fees can total 2% to 5% of the loan amount. Some lenders may charge application or documentation fees. Always ask for a detailed fee breakdown before committing.

How Does Loan Term Affect Home Equity Loan Costs?

Loan terms typically range from 5 to 30 years. Longer terms mean lower monthly payments but higher total interest paid. Shorter terms have higher payments but less interest overall. Choose a term that balances affordability with total loan cost.

Can Home Equity Loan Costs Vary By Credit Score?

Yes, credit scores significantly impact home equity loan costs. Higher scores usually qualify for lower interest rates and fees. Lower scores may lead to higher rates or loan denial. Maintaining a good credit score helps reduce overall loan expenses.

Conclusion

Home equity loans come with various costs to consider. Interest rates and fees affect the total amount you repay. It is important to compare offers from different lenders. Know the loan terms and payment schedules before deciding. Choosing wisely can save you money in the long run.

Use your home equity carefully and plan your budget well. Understanding the costs helps you make smart financial choices. A clear view of expenses avoids surprises later. Take time to learn and ask questions if unsure.