Are you thinking about tapping into your home’s value but aren’t sure which option fits you best? When it comes to borrowing against your home, two popular choices are home equity loans and cash-out refinancing.

Both let you access cash, but they work in very different ways. Understanding these differences can save you money and stress down the road. Keep reading to discover which option matches your needs and how to make the smartest move with your home’s equity.

Home Equity Loan Basics

A home equity loan lets you borrow money using your house as security. It uses the equity you have built in your home. Equity is the difference between your home’s value and what you owe on your mortgage.

This loan gives you a lump sum. You pay it back with fixed monthly payments over a set time. It is different from refinancing your mortgage or getting a cash-out refinance.

How Home Equity Loans Work

You apply for a loan based on your home equity. The lender checks your credit and home value. If approved, you get a fixed amount of money.

Payments include principal and interest. You pay the same amount every month until the loan ends. The loan is secured by your home, so missing payments can risk foreclosure.

Typical Terms And Rates

Home equity loans usually have terms from 5 to 30 years. Interest rates are often fixed and lower than credit cards or personal loans. Your rate depends on your credit score and home value.

Since the loan is secured, lenders offer better rates. You know your monthly payment from the start. This helps with budgeting.

When To Choose A Home Equity Loan

Choose a home equity loan for large, one-time expenses. Examples include home repairs, medical bills, or education costs. It works best if you want predictable payments and a fixed interest rate.

A home equity loan is not ideal for small or short-term needs. For flexible access to funds, other options may suit you better.

Credit: www.citizensbank.com

Cash Out Refinance Basics

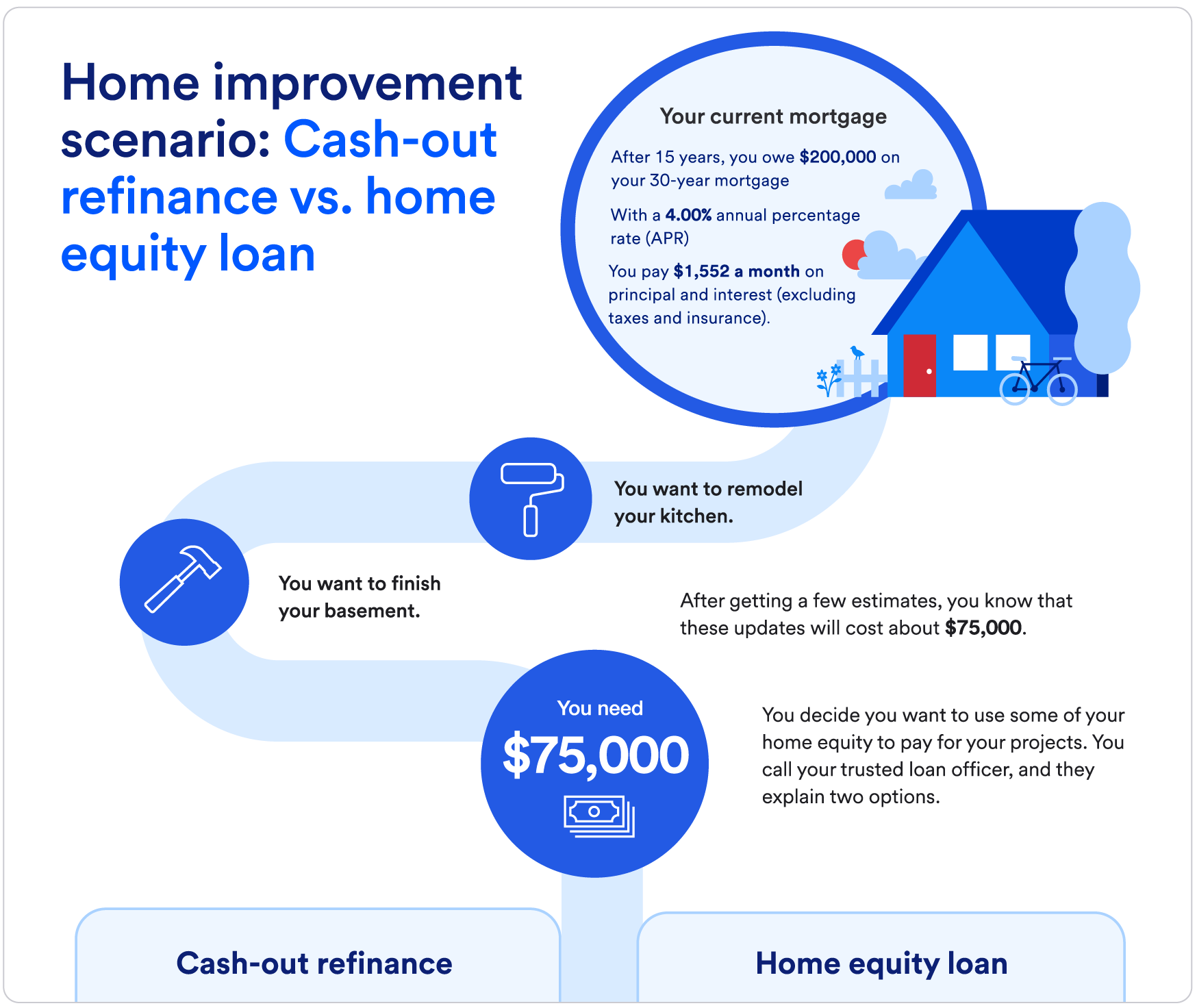

Cash out refinance is a popular way to use your home’s value. It lets you borrow money by replacing your current mortgage with a new, larger one. The extra cash can be used for many needs, such as home repairs or paying off debt.

This option changes your mortgage and gives you a lump sum of money. Understanding how it works helps you decide if it suits your financial goals.

How Cash Out Refinance Works

You apply for a new mortgage higher than your current loan. The lender pays off your old mortgage first. Then, you get the difference in cash. This amount depends on your home’s value and loan limits.

The process includes an appraisal to check your home’s worth. Approval depends on your credit score and income. You start paying the new loan with updated terms.

Loan Terms And Interest Rates

Cash out refinance usually offers fixed or adjustable rates. Interest rates might be lower than other loans. Loan terms can range from 15 to 30 years.

Longer terms mean lower monthly payments but more interest overall. Shorter terms have higher payments but save money on interest. Always compare rates before deciding.

Ideal Situations For Cash Out Refinance

This option fits well if you want to lower your mortgage rate. It works when you need a large sum of money at once. Using it to improve your home can increase property value.

Good credit and stable income make approval easier. Avoid using cash out refinance for everyday expenses or short-term needs.

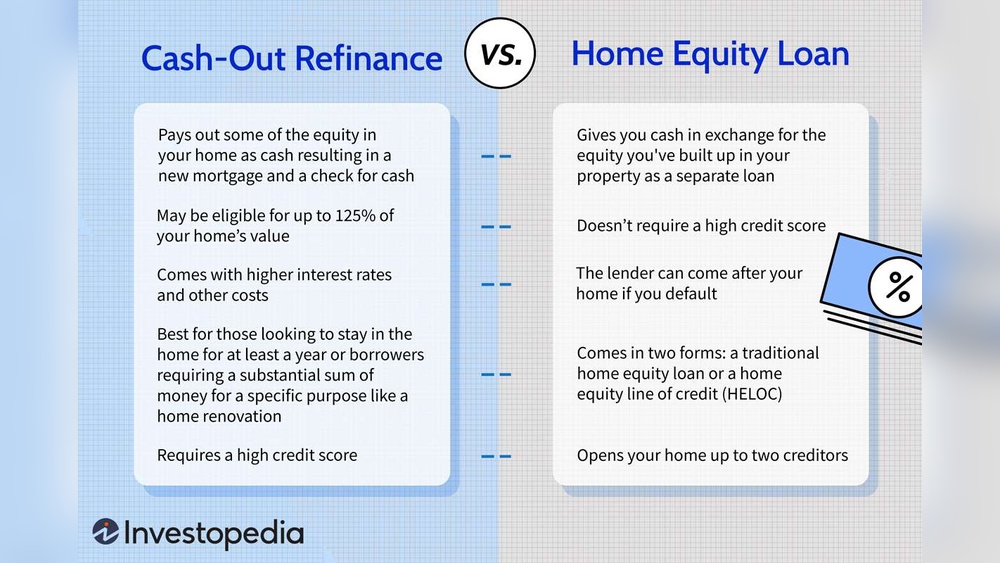

Key Differences

Understanding the key differences between a home equity loan and a cash-out refinance helps you choose the right option. Both let you use your home’s value for cash. Yet, they work in different ways. These differences affect your payments, interest rates, and fees.

Loan Structure Comparison

A home equity loan is a second loan on top of your mortgage. You get a fixed amount as a lump sum. You repay it with fixed monthly payments. A cash-out refinance replaces your current mortgage with a new, larger one. You get the difference in cash. The new loan covers your old mortgage and extra cash.

Impact On Monthly Payments

Home equity loans add a new monthly payment. Your original mortgage stays the same. Payments are separate. Cash-out refinance changes your mortgage payment. It can raise or lower your monthly cost. It depends on the new loan amount and interest rate.

Effect On Interest Rates

Home equity loans usually have higher interest rates than first mortgages. The rates are often fixed. Cash-out refinance interest rates tend to be lower. They are closer to your original mortgage rates. Rates can be fixed or adjustable.

Closing Costs And Fees

Home equity loans have lower closing costs. Fees are usually less than a refinance. Cash-out refinance costs more to close. You pay for appraisal, title, and loan fees. These costs can be added to your loan balance.

Benefits And Drawbacks

Choosing between a home equity loan and a cash-out refinance depends on your needs. Each option has benefits and drawbacks. Understanding these can help you make a better choice. Both use your home’s value but work differently. This section breaks down their pros and cons clearly.

Advantages Of Home Equity Loans

Home equity loans offer fixed interest rates. This means your payments stay the same. You get a lump sum of money upfront. The loan usually has a shorter term. This helps you pay it off faster. Interest rates are often lower than credit cards. You keep your original mortgage separate.

Disadvantages Of Home Equity Loans

These loans require good credit and home equity. Closing costs can be high. You must pay two separate monthly payments. The loan uses your home as collateral. Missing payments can risk your home. The amount you can borrow is limited.

Advantages Of Cash Out Refinance

This option replaces your old mortgage with a new one. You get extra cash from your home’s equity. It can lower your interest rate. One monthly payment instead of two. You can borrow a larger amount. It may help simplify your finances.

Disadvantages Of Cash Out Refinance

Refinancing resets your loan term. This can mean paying more interest over time. Closing costs may be costly. You risk losing your home if you default. The process takes longer than a home equity loan. Not all borrowers qualify easily.

Choosing The Right Option

Choosing between a home equity loan and a cash-out refinance depends on your personal financial situation. Each option has benefits and drawbacks. Understanding these can help you make a smart choice.

Financial Goals To Consider

Think about why you need the money. A home equity loan works well for specific costs, like home repairs or education. Cash-out refinance might be better for paying off higher interest debt or lowering monthly payments. Knowing your goal helps pick the right loan.

Credit Score And Qualification Factors

Your credit score affects loan approval. Home equity loans usually need good credit and steady income. Cash-out refinance might have stricter rules but can offer better rates. Check your credit score before applying to avoid surprises.

Long-term Financial Impact

Consider how each option affects your finances over time. Home equity loans keep your original mortgage intact. Cash-out refinance replaces your mortgage with a new one, possibly changing your monthly payment. Think about your budget and future plans before deciding.

Credit: www.usbank.com

Credit: www.directmortgageloans.com

Frequently Asked Questions

What Is A Home Equity Loan?

A home equity loan is a fixed-rate loan based on your home’s equity. It provides a lump sum with a set repayment term and interest rate. This loan is separate from your primary mortgage and is ideal for large, one-time expenses.

How Does Cash-out Refinance Work?

Cash-out refinance replaces your existing mortgage with a new, larger loan. You receive the difference in cash. This option often offers lower interest rates but resets your loan term. It’s useful for consolidating debt or funding major expenses.

Which Option Has Lower Interest Rates?

Cash-out refinance typically offers lower interest rates than home equity loans. This is because it replaces your original mortgage with a new one. Rates depend on credit score, loan amount, and market conditions. Always compare offers before deciding.

Can I Keep My Original Mortgage Term With A Home Equity Loan?

Yes, a home equity loan does not affect your original mortgage term. It acts as a second loan with its own repayment schedule. This allows flexibility if you want to maintain your current mortgage terms.

Conclusion

Choosing between a home equity loan and cash-out refinance depends on your needs. Home equity loans offer fixed rates and set payments. Cash-out refinance replaces your old mortgage with a new, larger one. Each has benefits and risks. Think about interest rates, loan terms, and fees.

Also, consider how long you plan to stay in your home. Knowing these differences helps you make a smart choice. Take time to compare both options carefully before deciding.