Are you curious about how equity release and lifetime mortgages work, but unsure which one suits your needs? Understanding the difference between these two options can make a big impact on your financial future.

Whether you’re looking to unlock cash from your home or plan your retirement, knowing the key details can help you make smart decisions. Keep reading to discover how equity release and lifetime mortgages differ—and find out which could be the right choice for you.

Equity Release Basics

Equity release lets older homeowners access cash from their property. It provides money without needing to sell the home. This helps people use their home’s value to support their needs in later life.

Understanding the basics of equity release is important. It helps you choose the right option for your situation. Two main ideas to know are the types of equity release and who can apply.

Types Of Equity Release

There are two main types of equity release: lifetime mortgage and home reversion. A lifetime mortgage is a loan secured on your home. You keep ownership and repay when you die or move out.

Home reversion means selling a part or all of your home to a company. You get cash now but live rent-free until you die or move permanently. The company then owns that share of the property.

Eligibility Criteria

To qualify, you usually must be 55 or older. Your home must be your main residence. Lenders check the property’s value and condition. You must not have other large debts secured on your home.

Each product has specific rules. Some need you to live in England or Wales. Others allow shared ownership or more flexible repayment options.

Typical Uses

People use equity release to pay for home improvements. Others cover daily living costs or medical bills. It can help fund holidays or support family members financially.

It also offers peace of mind by providing extra income in retirement. Many use it to reduce mortgage payments or clear debts.

Credit: everyinvestor.co.uk

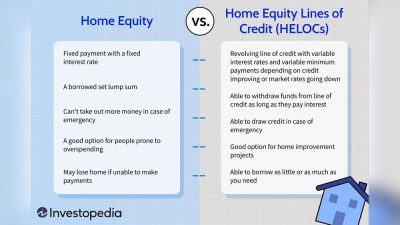

Lifetime Mortgage Explained

A lifetime mortgage is a popular type of equity release. It lets homeowners over 55 borrow money against their home. You keep living in your house without monthly payments. The loan and interest are paid back when you die or move into long-term care.

This option helps people use their home’s value without selling it. The amount you borrow depends on your age and home value. It is a way to get cash while staying in your home.

How Lifetime Mortgages Work

You borrow money secured against your property. The lender pays you a lump sum or regular payments. You still own your home and live there as usual. Interest builds up over time and adds to the loan. The total debt is repaid when the house is sold after you pass away or move out.

Repayment Options

You do not make monthly repayments during your lifetime. The loan and interest grow and are paid later. Some plans let you pay interest monthly to reduce the total debt. Repayment happens after death or moving to care. The house is sold, and the lender is paid from the sale proceeds.

Pros And Cons

The main benefit is accessing money without moving home. No monthly payments can ease financial pressure. Interest compounds, so the debt can grow large over time. Your home’s value must cover the loan when repaid. It may reduce the inheritance left to family. Good advice is important before choosing this option.

Comparing Key Features

Equity release and lifetime mortgages both help older homeowners access cash from their homes. They share some features but differ in important ways. Understanding these key features helps you choose the right option.

Loan Structure

Equity release is a broad term for ways to take money from your home. A lifetime mortgage is one type of equity release. With a lifetime mortgage, you borrow a lump sum or smaller amounts. You keep full ownership of your home. You do not make monthly repayments. The loan is repaid when you pass away or move into long-term care.

Interest Accumulation

Interest builds up on lifetime mortgages over time. It adds to the total amount you owe. You do not pay interest each month. Instead, it rolls up until the loan ends. This means the debt grows faster if you live longer. Equity release plans may have different interest setups, but lifetime mortgages always have this roll-up feature.

Impact On Inheritance

Both equity release and lifetime mortgages reduce the value of your estate. The money you owe is paid from your home’s sale. This leaves less money for your heirs. You can choose options to protect some inheritance. Talking with a financial advisor helps protect your family’s future.

Credit: www.moneyrelease.co.uk

Costs And Fees

Understanding the costs and fees of equity release and lifetime mortgages helps you make smart choices. These financial products have different charges that affect your money over time. Knowing these costs clearly helps avoid surprises later.

Upfront Charges

Equity release and lifetime mortgages have initial fees. These include valuation fees, legal costs, and arrangement fees. Usually, lifetime mortgages have higher upfront charges. These fees cover the house value check and paperwork. Some providers may offer deals with lower or no upfront fees.

Ongoing Costs

Both products may have ongoing fees. These include interest on the loan and annual management fees. Interest builds up over time, increasing the amount owed. Lifetime mortgages often charge a fixed or variable interest rate. Equity release plans might have monthly or yearly service fees. These costs reduce your home’s remaining value.

Early Repayment Penalties

Paying off your loan early can lead to penalties. Many lifetime mortgages have early repayment charges for several years. These fees can be a percentage of the amount repaid. Equity release plans sometimes have similar penalties. Check terms carefully before signing. Early repayment penalties protect lenders but can cost you.

Risks And Considerations

Understanding risks and considerations is key before choosing equity release or a lifetime mortgage. Both options affect your finances and future plans. Knowing the possible downsides helps you make a smart decision. Here are some important points to think about.

Effect On Benefits

Taking out equity release or a lifetime mortgage might reduce your benefits. Some income-based benefits depend on your savings and income. Extra money from these plans could push you above the limit. This might lower or stop payments like Pension Credit or Housing Benefit.

Property Value Changes

House prices can go up or down over time. If your property’s value falls, you might owe more than it is worth. Some lifetime mortgages have a “no negative equity” guarantee. This means you will never owe more than your home’s value when sold. But not all plans offer this, so check carefully.

Eligibility Limitations

Not everyone can use equity release or lifetime mortgages. Lenders usually require you to be at least 55 years old. Your home must meet certain conditions too. Some properties may not qualify. Also, some health issues might affect eligibility or terms.

Credit: www.waldrons.co.uk

Choosing The Right Option

Choosing the right option between equity release and a lifetime mortgage depends on several important factors. Understanding your needs helps you make a smart decision. Both options let you access money tied up in your home. Yet, they work differently and suit different situations.

Financial Goals

Think about what you want to achieve with the money. Need cash for home repairs? Or want to boost your retirement income? Equity release may offer a lump sum or smaller payments. A lifetime mortgage usually gives a lump sum or regular income. Your goals guide the best choice for your money needs.

Personal Circumstances

Your age, health, and family situation matter. Some plans have age limits or health checks. Consider how long you plan to stay in your home. Also, check if you want to leave money for heirs. Personal details affect which option fits your life best.

Seeking Professional Advice

Talk to a financial adviser or specialist before deciding. Experts explain costs, risks, and benefits clearly. They help you understand complex terms and conditions. Good advice ensures you pick a safe and suitable product. This step protects your future finances and peace of mind.

Frequently Asked Questions

What Is Equity Release In Simple Terms?

Equity release lets homeowners access cash by unlocking their property’s value. It suits those aged 55 or over. The loan is repaid after they move or pass away. It offers financial flexibility without monthly repayments.

How Does A Lifetime Mortgage Work?

A lifetime mortgage is a type of equity release. You borrow against your home’s value while living there. Interest builds up and is repaid when you die or move out. It allows you to keep ownership of your property.

What Are The Main Differences Between Equity Release And Lifetime Mortgage?

Equity release is a broad term covering products to unlock home value. A lifetime mortgage is a specific equity release product. Lifetime mortgage involves a loan with interest, repaid later. Other equity release types may differ in terms and repayment.

Is Equity Release Suitable For All Homeowners?

Equity release suits homeowners aged 55+ with significant home equity. It’s not ideal if you plan to move soon. It can affect benefits and inheritance, so advice is essential before proceeding.

Conclusion

Equity release and lifetime mortgages help you access money from your home. Equity release is a broad term that includes lifetime mortgages. Lifetime mortgages let you borrow a fixed amount, keeping ownership of your home. Both options have pros and cons to consider.

Think about your financial needs and future plans. Speak with a trusted advisor to understand what suits you best. Taking time to compare will help you make the right choice. Your home can support your finances, but choose carefully.