Are you thinking about tapping into your home’s value but not sure whether a home equity loan or a line of credit is the right choice for you? Making the right decision can save you money and stress down the road.

Each option has its perks and pitfalls, and what works best depends on your unique needs and goals. Keep reading, and you’ll discover which one fits your situation perfectly—so you can move forward with confidence and control.

Home Equity Loan Basics

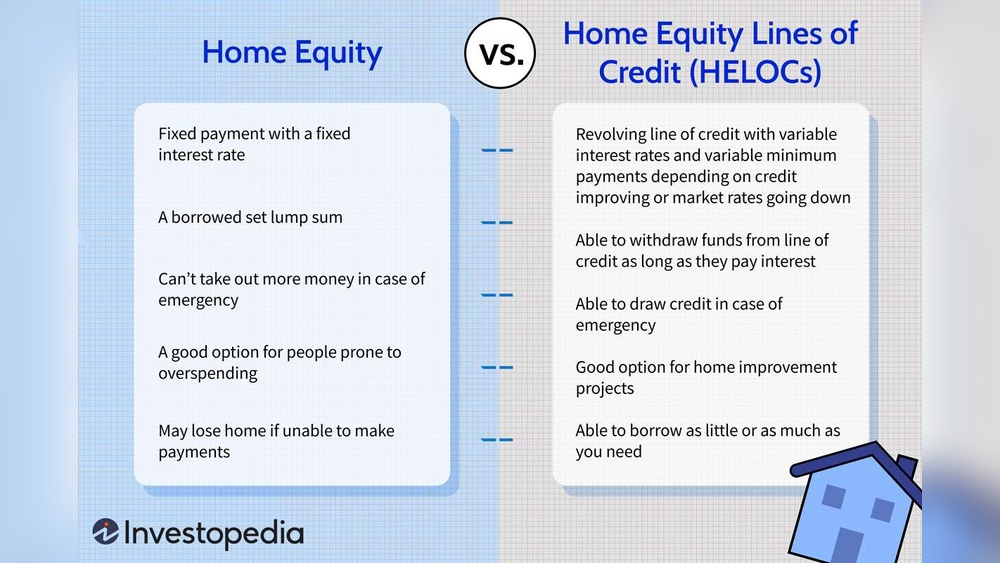

Understanding home equity loans helps you decide on the right borrowing option. These loans let homeowners use their home’s value as collateral. They provide a lump sum of money that you repay over time. Knowing the basics makes it easier to compare with other choices.

What Is A Home Equity Loan?

A home equity loan is a fixed amount of money borrowed against your home’s value. It works like a second mortgage. You get the money all at once. Then, you repay it in monthly payments over a set period.

How Home Equity Loans Work

The loan amount depends on your home’s equity. Equity is the home’s current value minus what you owe on it. You must qualify based on your credit and income. After approval, you receive the money at one time. You repay with fixed monthly payments including interest and principal.

Typical Terms And Rates

Home equity loans usually have terms from 5 to 30 years. Interest rates are often fixed, so payments stay the same. Rates depend on your credit score and market conditions. Fixed rates help with budgeting monthly expenses. Some lenders may charge fees for application or closing.

Credit: www.citizensbank.com

Home Equity Line Of Credit (heloc) Basics

Understanding a Home Equity Line of Credit (HELOC) helps in deciding the right home loan option. This type of loan lets homeowners use their home’s value to borrow money. It works differently from a regular loan. Let’s explore the basics of HELOC.

What Is A Heloc?

A HELOC is a loan that uses your home’s equity as collateral. It acts like a credit card with a borrowing limit. You can borrow money, pay it back, and borrow again. This makes it flexible for many expenses.

How Helocs Function

You get a set borrowing limit based on your home’s value. You can withdraw money anytime during the draw period. Monthly payments may vary because of changing balances and interest rates. After the draw period, repayment begins on the amount borrowed.

Common Terms And Rates

HELOCs usually have variable interest rates that change over time. The draw period lasts 5 to 10 years, often followed by 10 to 20 years of repayment. Lenders may charge fees like appraisal, application, or annual fees. It’s important to know these before borrowing.

Comparing Costs And Interest Rates

Comparing costs and interest rates helps you choose the right option. Both home equity loans and lines of credit have different costs. Understanding these differences saves money and avoids surprises. Interest rates and fees play a big role in the total cost. Knowing how these work makes decision easier.

Fixed Vs Variable Rates

Home equity loans usually have fixed interest rates. This means your monthly payment stays the same. Fixed rates make budgeting simple and stable. Home equity lines of credit (HELOCs) often have variable rates. These rates can go up or down over time. Variable rates may start lower but can rise later. Choose fixed rates if you want steady payments. Variable rates suit those who can handle changing costs.

Fees And Closing Costs

Home equity loans often have higher upfront fees. These include appraisal, application, and closing costs. The fees add to the initial expense of the loan. HELOCs usually have lower or no closing costs. Some lenders charge annual fees or inactivity fees for HELOCs. Watch out for these ongoing costs. Check all fees before deciding. Lower fees can save money over time.

:max_bytes(150000):strip_icc()/dotdash_Final_Home_Equity_Loan_vs_HELOC_What_the_Difference_Apr_2020-01-af4e07d43f454096b1fbad8cfe448115.jpg)

Credit: www.investopedia.com

Repayment Flexibility

Repayment flexibility is a key factor when choosing between a home equity loan and a line of credit. It affects how easily you can manage your monthly payments and overall debt. Understanding these differences helps you pick the best option for your budget and needs.

Payment Structures

Home equity loans have fixed monthly payments. Each payment includes principal and interest. This makes budgeting easier. You know the exact amount to pay every month. A home equity line of credit (HELOC) has variable payments. Your monthly payment can change. It depends on how much you borrow and the interest rate. You may pay interest only at first. Then, payments increase when you repay the principal. This can be less predictable but offers more control.

Draw And Repayment Periods

With a home equity loan, you receive the full loan amount at once. You start repaying right away. Repayment periods usually last 10 to 30 years. HELOCs have two phases: draw and repayment. During the draw period, you can borrow as needed. You usually pay only interest. After this, the repayment period begins. You must pay back both principal and interest. Draw periods last about 5 to 10 years. Repayment may take 10 to 20 years. This setup offers more flexibility but requires careful planning.

Best Uses For Each Option

Choosing between a home equity loan and a home equity line of credit (HELOC) depends on your needs. Both options let you borrow money using your home’s value. Each works best in different situations. Understanding these uses helps you pick the right one.

When To Choose A Home Equity Loan

Choose a home equity loan for a large, one-time expense. It gives you a fixed amount of money at a set interest rate. This works well for home repairs, debt consolidation, or big purchases. You get predictable monthly payments. You know exactly how much to pay each month. This loan suits people who want stability in payments.

When To Choose A Heloc

A HELOC is best for ongoing or flexible spending. It works like a credit card with a credit limit. Use it for multiple expenses over time. Examples include home renovations done in stages or college fees. You borrow money as needed and pay interest only on what you use. This option fits people who want flexibility and control over borrowing.

Risks And Considerations

Choosing between a home equity loan and a line of credit involves risks and important factors. Understanding these risks helps protect your home and finances. Both options use your home as security. This means you must be sure you can repay the money.

Each choice affects your financial situation differently. Thinking about these risks helps you make a better decision. Here are key points to consider.

Impact On Home Ownership

Both loans use your home as collateral. Missing payments can lead to losing your home. This risk makes timely repayment very important.

A home equity loan gives you a lump sum. You repay it with fixed monthly payments. This can make budgeting easier.

A home equity line of credit lets you borrow as needed. Payments may vary depending on how much you use. This can be harder to manage.

Both types can reduce your home’s equity. Less equity means less value if you sell later. Consider how much equity you want to keep.

Credit And Financial Factors

Both loans affect your credit score. Late payments lower your score and increase costs. Paying on time helps build better credit.

Home equity loans have fixed interest rates. Your monthly payments stay the same. This offers stability in your budget.

Lines of credit often have variable rates. Payments can rise or fall over time. This can cause surprises in your bills.

Think about your ability to repay. Avoid borrowing more than you can handle. Overextending credit can cause long-term problems.

Application Process Tips

Applying for a home equity loan or line of credit can feel confusing. Knowing what to expect helps you prepare well. This section gives tips on the application process. It covers what you need to qualify and what documents to have ready. These tips make the process smoother and faster.

Qualifying Requirements

Lenders check your credit score and income. They want to see steady income and low debt. Your home must have enough equity for the loan. Usually, lenders want at least 15% to 20% equity. A good credit score improves your chances. The debt-to-income ratio also matters. It should be below 43%. Meeting these rules makes approval easier.

Documentation Needed

Prepare several key documents before you apply. Proof of income like pay stubs or tax returns is essential. Lenders also ask for bank statements to check savings. Your homeowner’s insurance and property tax bills may be needed. A recent home appraisal might be required too. Have these papers organized and ready to share. This speeds up the review and approval steps.

Expert Recommendations

Experts suggest careful thinking before choosing between a home equity loan or line of credit. Each option fits different needs and situations. Knowing your financial goals and seeking advice helps make the best choice.

Assessing Your Financial Goals

Start by listing your main financial needs. Are you planning a one-time expense or ongoing costs? A home equity loan suits fixed costs with a clear budget. A line of credit works well for flexible spending over time. Understanding your goals guides your decision. It helps avoid surprises later.

Consulting Professionals

Talk to financial advisors or mortgage experts. They explain terms and risks clearly. Professionals review your income, debts, and credit score. Their insights show which option fits your situation best. They also help spot hidden fees and interest rates. Getting expert advice saves money and stress.

Credit: www.experian.com

Frequently Asked Questions

What Is The Main Difference Between A Home Equity Loan And Heloc?

A home equity loan provides a lump sum with fixed interest rates. A HELOC offers a credit line with variable rates, allowing flexible borrowing.

Which Option Has Lower Interest Rates, Loan Or Line Of Credit?

Home equity loans usually have fixed rates, which may be higher initially. HELOCs often start with lower variable rates but can increase over time.

Can I Use A Home Equity Line For Multiple Expenses?

Yes, a HELOC lets you borrow funds repeatedly during the draw period. It’s ideal for ongoing or multiple home improvement projects.

Which Is Better For Budgeting: Loan Or Line Of Credit?

A home equity loan is better for fixed budgets due to predictable payments. HELOC payments vary, making budgeting less certain.

Conclusion

Choosing between a home equity loan and a line of credit depends on your needs. A loan offers a fixed amount and steady payments. A line of credit gives flexible access to money anytime. Think about your budget and how you plan to use the funds.

Compare interest rates and repayment terms carefully. Both have pros and cons to fit different situations. Take your time to decide what suits you best. This helps avoid surprises and keeps your finances safe.