Are you curious about how equity release works in the UK and whether it could be the right choice for you? Unlocking the value tied up in your home might seem complicated, but it doesn’t have to be.

Understanding how equity release works can open new financial opportunities, giving you extra cash without the need to move. You’ll discover simple explanations and clear steps to help you see if equity release fits your needs—and how it can provide the financial freedom you’re looking for.

Keep reading to find out how your home could become a valuable resource for your future.

Basics Of Equity Release

Equity release helps homeowners access money tied up in their property. It works by turning part of your home’s value into cash. This option suits people aged 55 or older. The money can support retirement, pay debts, or cover other costs.

Understanding the basics is key. It avoids surprises and helps you make better choices. Learn what equity release means and the types of plans available.

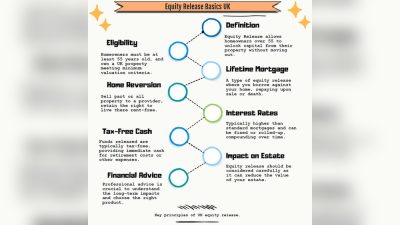

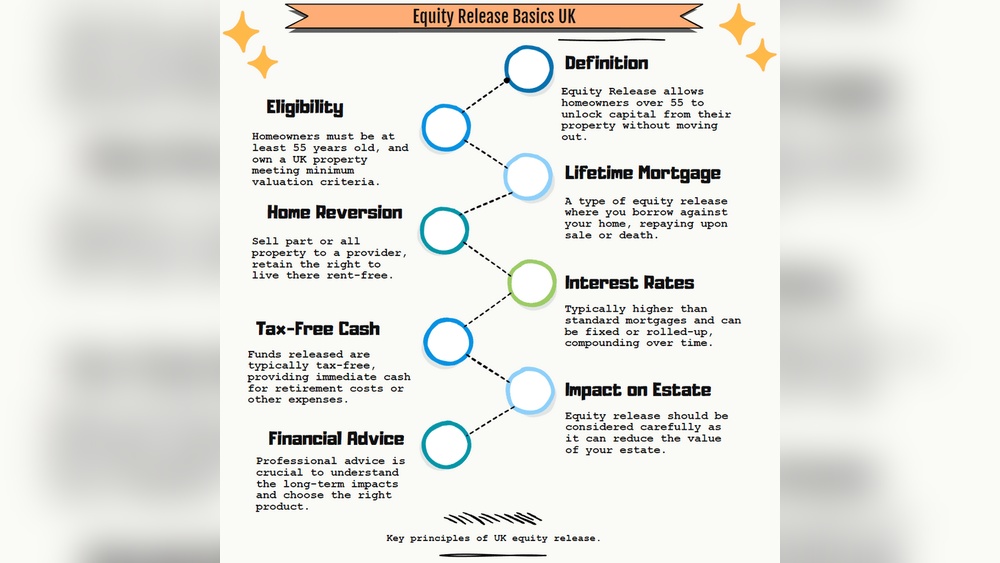

What Is Equity Release

Equity release is a way to get cash from your home. You do not have to sell the house. Instead, you borrow money against your property’s value. The loan and interest are paid back after you die or move into care. This means no monthly repayments are needed during your lifetime. It keeps your home ownership but reduces your estate value.

Types Of Equity Release Plans

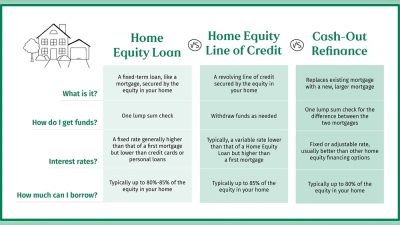

Two main types exist: lifetime mortgage and home reversion. Lifetime mortgage is the most popular. You borrow a lump sum or smaller amounts over time. Interest builds up but is not paid until the end. With home reversion, you sell part or all of your home. You live there rent-free or pay a low rent. You or your family keep the rest of the property.

Each plan has pros and cons. Costs, flexibility, and impact on inheritance vary. Choose carefully based on your needs and situation.

Eligibility Criteria

Equity release allows homeowners to access money tied up in their property. Not everyone qualifies. There are rules to follow. These rules help lenders decide who can get equity release. Understanding these rules helps you know if you qualify.

Age Requirements

Most equity release plans need you to be at least 55 years old. Some lenders may set the minimum age at 60 or higher. The older you are, the easier it is to qualify. Age affects how much money you can borrow.

Property Conditions

Your home must be in good shape. Lenders check if the house is safe and well-maintained. The property usually must be your main home. Some types of homes, like flats or new builds, may not qualify.

Financial Considerations

Lenders look at your income and debts. They want to be sure you can afford any fees or interest. Your financial situation helps decide the amount you can release. No need for income proof in some plans, but it varies.

How Equity Release Unlocks Wealth

Equity release lets homeowners access the money tied up in their property. It offers cash without selling the home. This option suits people aged 55 or older who want extra funds for life needs. Understanding how equity release works helps in making smart decisions.

The process involves several key steps. Each affects how much money you receive and what happens later. Let’s explore how equity release unlocks wealth through your home.

Calculating Your Home’s Value

Your home’s value sets the starting point. A professional surveyor estimates the current market price. This amount decides how much equity you can use. Prices vary by location and house condition. Higher value means more potential cash.

Loan Amount And Interest Rates

The loan amount depends on your home’s value and age. Older homeowners often access a larger share. Interest rates affect the total repayment sum. Rates can be fixed or variable, changing costs over time. Interest usually adds up and is paid later.

Impact On Inheritance

Equity release reduces the home’s value left to heirs. The loan and interest repay after you pass away or move out. This means less money for your family. Planning helps balance current needs and inheritance goals.

Benefits Of Equity Release

Equity release offers several benefits for homeowners aged 55 and over. It allows access to money tied up in a property without the need to sell or move. This financial option helps improve day-to-day money matters and future security.

Accessing Cash Without Moving

Equity release lets you get cash from your home without changing your address. You can stay in your house and enjoy the comfort you know. This means no need to find a new place or deal with moving costs. The money can help with home repairs, holidays, or paying off debts.

Flexible Repayment Options

Repayments on equity release plans are flexible to suit your needs. Some plans let you pay interest during your lifetime. Others add the debt to the loan and repay it later. This means no monthly payments if you do not want to make them. The loan is usually repaid when you die or move into care.

Improving Financial Security

Using equity release can boost your financial security in later years. It provides extra funds to cover unexpected costs or daily expenses. This support can reduce money worries and improve quality of life. It helps you maintain independence and live comfortably at home.

Risks And Drawbacks

Equity release can help access money from your home. It sounds useful but carries risks and drawbacks. Understanding these risks helps make better decisions. Some may affect your money, benefits, and family plans. Be aware of these before proceeding.

Effect On Benefits And Taxes

Releasing equity may reduce your claim to some benefits. Income-based benefits might be affected by extra cash. It could change your tax situation too. Always check with a benefits advisor before applying. Tax rules can be complex and change often.

Interest Accumulation Over Time

Interest builds up on the amount you borrow. It is added to the loan and grows over time. The longer you keep the loan, the more you owe. This can reduce the money left for you or your family. Make sure to understand how interest works in your plan.

Impact On Estate And Inheritance

Equity release reduces the value of your estate. It means less inheritance for your family or heirs. Your home may need to be sold to repay the loan. This can affect your family’s future financial security. Talk to your loved ones and plan carefully.

Credit: sovereignboss.co.uk

Choosing The Right Equity Release Plan

Choosing the right equity release plan is important. It affects your finances and future. Equity release lets you access money from your home. But not all plans are the same. Understanding options helps you make a good choice. This guide explains how to pick the best plan for you.

Comparing Lifetime Mortgages And Home Reversion

Lifetime mortgages let you borrow money using your home as security. You keep full ownership of your property. Interest builds up over time, paid when you die or move out. Home reversion means selling part of your home. You get cash upfront but own less of your property later. Each has pros and cons. Think about how long you plan to stay in your home.

Getting Independent Advice

Seek advice from a qualified equity release specialist. Independent experts explain options clearly. They check if equity release fits your needs. Avoid decisions based on sales pressure. Good advice helps you avoid risks. It ensures you understand costs and effects on inheritance.

Evaluating Providers

Choose providers with good reputations and clear terms. Compare interest rates and fees carefully. Look for providers with strong customer support. Check reviews and ratings from past customers. Reliable providers follow government rules and guidelines. This protects your money and rights.

Application Process

The application process for equity release in the UK involves clear steps. It ensures you understand the product and get the best deal for your needs. Each stage is important to secure the right amount of money from your home.

Initial Assessment

The first step is the initial assessment. A specialist reviews your financial situation and home details. This helps decide if equity release suits your needs. They explain the types of plans available and answer your questions. No pressure, just clear information to help you decide.

Valuation And Offers

Next, your property gets a professional valuation. This shows how much money you can release. The lender uses this value to create an offer. You receive the offer in writing, showing the loan amount and terms. You can take time to review it carefully.

Legal Formalities

Legal work follows the offer acceptance. A solicitor explains the contract and checks all paperwork. They ensure you understand your rights and responsibilities. The solicitor handles the signing and registers the agreement with the land registry. This step protects your interests and finalizes the deal.

Credit: www.youtube.com

Credit: www.premierjobsuk.com

Frequently Asked Questions

What Is Equity Release And How Does It Work?

Equity release lets homeowners unlock property value without selling. It provides tax-free cash using your home as security. You keep living there, and repay later, usually on moving or passing away.

Who Is Eligible For Equity Release In The Uk?

Typically, UK homeowners aged 55+ qualify for equity release. The property must be your main residence with sufficient value. Lenders assess your situation to ensure suitability and affordability.

What Are The Main Types Of Equity Release Plans?

The two main types are lifetime mortgages and home reversion plans. Lifetime mortgages charge interest on the loan amount. Home reversion sells a share of your home for cash.

How Does Equity Release Affect Inheritance And Estate?

Equity release reduces your property’s value, affecting inheritance. The loan and interest are repaid from your home’s sale after death or moving out. This may reduce the estate left to heirs.

Conclusion

Equity release helps homeowners access money from their property. It works by turning part of your home’s value into cash. You keep living in your house while receiving money. The loan is paid back when you sell or pass away.

This option suits older people needing extra funds. Always get advice from a trusted financial expert. Understand all terms before making a decision. Equity release can ease money worries in later life. Think carefully and choose what fits your needs best.