Thinking about tapping into your home’s value with a home equity loan? Before you take that step, it’s important to understand what you’re getting into.

This type of loan can be a powerful tool for funding big expenses, but it also comes with risks that could affect your financial future. You’ll discover the key things you need to know to make a smart decision. Keep reading to protect your investment and avoid common pitfalls that many homeowners face.

Your home and your wallet will thank you.

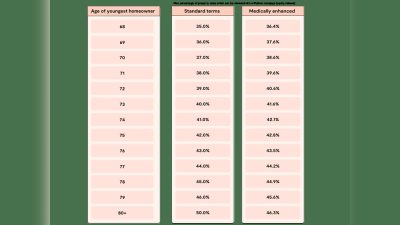

Credit: www.experian.com

Home Equity Loan Basics

Understanding the basics of a home equity loan is important before applying. This type of loan lets you borrow money using your home’s value. It can be helpful for big expenses or debt consolidation. Knowing how it works, the types available, and who qualifies helps you make smart choices.

How Home Equity Loans Work

A home equity loan uses your home’s equity as security. Equity is the difference between your home’s market value and what you owe. You borrow a fixed amount and repay it over time with interest. The interest rate is often lower than other loans. Payments are usually monthly and fixed, making budgeting easier.

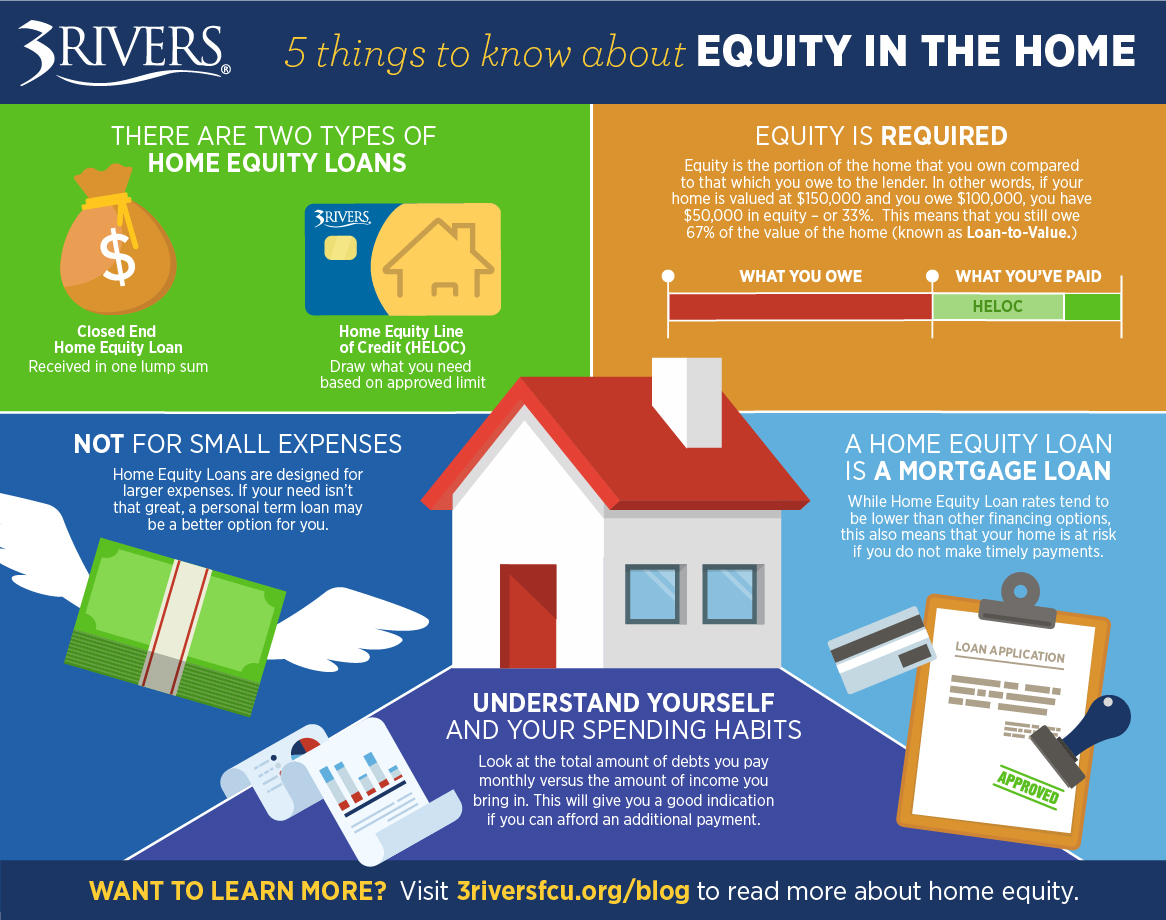

Types Of Home Equity Loans

There are two main types: lump-sum loans and home equity lines of credit (HELOC). Lump-sum loans give you all the money at once. HELOCs work like a credit card with a borrowing limit. You can borrow and repay multiple times during the draw period. Each type fits different financial needs and spending plans.

Eligibility Criteria

Lenders check your credit score, income, and debts to decide eligibility. You need enough equity in your home, usually 15% to 20%. Stable income shows you can repay the loan. Good credit helps you get better rates. Lenders also verify your home’s value with an appraisal. Meeting these rules increases your chances of approval.

Financial Considerations

Before taking a home equity loan, consider your financial situation carefully. This type of loan uses your home as security. It can help with big expenses but also adds risk. Knowing the costs and effects on your budget helps avoid surprises. Think about how the loan fits your money plans and goals.

Interest Rates And Fees

Home equity loans usually have fixed interest rates. This means your payments stay the same over time. Rates depend on your credit score and the market. Besides interest, watch for fees like application, appraisal, and closing costs. These fees can add up and increase the loan cost. Always ask for a clear list of all charges.

Impact On Monthly Budget

Monthly payments include principal and interest. Calculate if you can afford these payments comfortably. Missing payments can lead to losing your home. Consider your income stability before borrowing. A loan may reduce money for other needs or emergencies. Plan your budget to keep finances balanced.

Tax Implications

Interest on home equity loans may be tax-deductible. This depends on how you use the loan money. Using the loan for home improvements often qualifies for deductions. Using it for other expenses may not. Check current tax laws or ask a tax professional. This knowledge can save money when filing taxes.

Application Process

Applying for a home equity loan involves several clear steps. Knowing the process helps you prepare and avoid delays. The lender checks your financial health and property value. This section explains what you must do to complete the application.

Required Documentation

You need proof of income, such as pay stubs or tax returns. Lenders also ask for recent bank statements. Prepare documents showing your home’s value, like an appraisal report. Identification proof, such as a driver’s license, is necessary. Having these ready speeds up your application.

Credit Score Requirements

Lenders review your credit score to decide approval. Scores above 620 usually qualify for home equity loans. Higher scores get better interest rates. Scores below 620 may face higher costs or rejection. Check your credit score before applying to avoid surprises.

Approval Timeline

The approval process can take from a few days to several weeks. It depends on how fast you provide documents. The lender also needs time to appraise your home. Quick responses help speed up approval. Plan for at least two weeks before receiving funds.

Credit: www.esl.org

Risks And Benefits

Home equity loans let you borrow money using your house as security. They offer a way to fund big expenses or consolidate debt. Still, they come with risks that need thought. Understanding both sides helps you decide wisely.

Potential Risks

Failing to repay can lead to losing your home. Interest rates may rise, increasing monthly payments. You might borrow more than you can afford. Loan fees and closing costs add to the expense. Using your home as collateral means high stakes.

Advantages Of Home Equity Loans

These loans usually have lower interest rates than credit cards. They provide a lump sum, useful for big projects. Fixed rates mean your payment stays the same. Interest may be tax-deductible, lowering your costs. They can improve your credit score if paid on time.

Alternatives To Consider

Personal loans do not use your home as security. Credit cards offer quick access but have high rates. Home equity lines of credit give flexible borrowing options. Refinancing your mortgage might lower your overall rate. Each option has pros and cons for different needs.

Maximizing Loan Value

Getting a home equity loan can offer many benefits. It is important to use the loan wisely to get the best value. Smart planning helps you avoid wasting money and increases your home’s worth. Spending the loan on the right projects can save you money in the long run. Using the funds carefully ensures you meet your financial goals and keep your home secure.

Smart Uses For Loan Funds

Use the loan to pay off high-interest debt. This saves money on interest payments. You can also fund education or start a small business. These uses help improve your financial future. Avoid spending on short-term wants. Focus on projects that bring lasting benefits.

Improving Home Value

Invest in repairs and upgrades that raise your home’s price. Kitchen and bathroom remodels often increase value. Energy-efficient improvements lower utility bills and attract buyers. Fix structural problems to avoid costly damage later. Choose projects that fit your budget and neighborhood standards.

Avoiding Common Pitfalls

Do not borrow more than you can repay. Missing payments can hurt your credit and risk your home. Avoid using loan money for vacations or cars. These do not add value and create debt. Always have a repayment plan before taking the loan. Keep loan terms clear and understand fees involved.

Credit: www.3riversfcu.org

Frequently Asked Questions

What Is A Home Equity Loan And How Does It Work?

A home equity loan lets you borrow against your home’s value. You get a lump sum and repay with fixed interest over time. It’s ideal for large expenses like renovations or debt consolidation.

How Much Can I Borrow With A Home Equity Loan?

Lenders typically allow borrowing up to 80-85% of your home’s appraised value minus your mortgage balance. The exact amount depends on your credit, income, and lender policies.

What Are The Risks Of A Home Equity Loan?

If you fail to repay, the lender can foreclose on your home. Interest rates may rise if you have a variable loan. Borrow only what you can afford to avoid financial trouble.

How Does A Home Equity Loan Affect My Credit Score?

Applying may cause a small credit score dip due to a hard inquiry. Timely payments can improve your credit over time. Missing payments can seriously harm your credit rating.

Conclusion

A home equity loan can help with big expenses or debt. Know the loan terms and interest rates before deciding. Think about your ability to make monthly payments. Remember, your house serves as loan security. Consider all costs, including fees and taxes.

Talk to a trusted lender or financial advisor. Take your time to compare different loan options. Make sure this loan fits your financial goals. Stay informed and careful to avoid future problems. Your home is valuable—treat this decision with care.