Are you thinking about tapping into your home’s value but aren’t sure whether a Home Equity Loan or a HELOC is right for you? Making the wrong choice could cost you more money or leave you stuck with terms that don’t fit your needs.

This guide will help you understand the key differences, so you can feel confident about your decision. Keep reading to discover which option matches your financial goals and lifestyle perfectly.

Home Equity Loan Basics

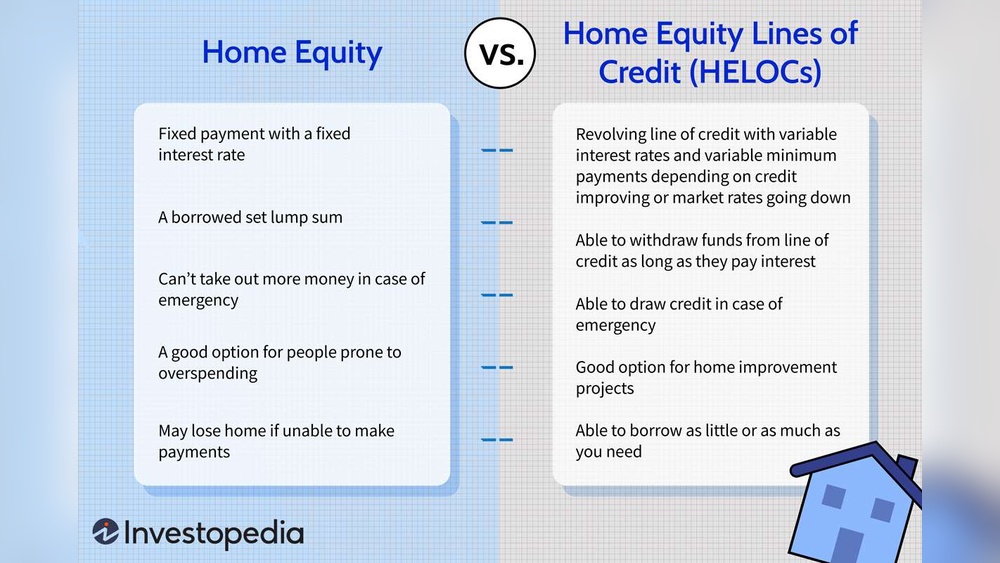

A home equity loan lets you borrow money using your house as security. This loan is different from other loans because it uses the value of your home. You get a set amount of money at one time. Many people use it for big expenses, like home repairs or paying off debt.

The loan amount depends on how much equity you have in your home. Equity is the difference between your home’s value and what you owe on it. Understanding the basics helps you decide if this loan fits your needs.

Fixed Interest Rates

Home equity loans usually have fixed interest rates. This means your rate stays the same for the entire loan period. You will know exactly how much interest you pay each month. This helps with budgeting and avoids surprises.

Lump Sum Disbursement

You receive the loan amount in one lump sum. This means you get all the money at once. You can use it right away for your planned expenses. There is no need to apply for more money later.

Repayment Terms

Repayment terms are usually set for 5 to 30 years. You make fixed monthly payments during this time. Each payment includes principal and interest. Paying on time helps protect your credit score and home ownership.

Heloc Essentials

A HELOC, or Home Equity Line of Credit, is a flexible way to borrow money using your home’s equity. It works like a credit card but uses your house as security. Understanding its key features helps you decide if it fits your needs.

Here are the basics that make a HELOC different from other loans.

Variable Interest Rates

HELOCs often have variable interest rates. This means your rate can change over time. It may start low but can rise or fall with the market. This affects your monthly payments. You should be ready for possible rate increases.

Revolving Credit Line

A HELOC gives you a revolving credit line. You can borrow money again as you repay it. This makes it good for ongoing expenses or emergencies. You only pay interest on what you use. This keeps costs lower than a fixed loan.

Draw And Repayment Periods

HELOCs have two phases: the draw period and the repayment period. During the draw period, you can borrow and pay interest only. After it ends, you must repay the loan principal and interest. The draw period usually lasts 5 to 10 years.

Comparing Costs

Comparing costs helps you choose the best option for your needs. Home equity loans and HELOCs have different cost structures. Understanding these differences can save you money and stress. This section breaks down key cost factors to consider before deciding.

Interest Rate Differences

Home equity loans usually have fixed interest rates. This means your payments stay the same every month. HELOCs often have variable rates that can change over time. Variable rates may start lower but can rise later. Fixed rates offer stability. Variable rates offer flexibility but less predictability.

Fees And Closing Costs

Home equity loans often come with higher fees upfront. These may include appraisal, application, and closing costs. HELOCs generally have lower initial fees but may charge annual fees. Some HELOCs also have draw fees when you take money out. Check all fees carefully before deciding.

Tax Implications

Interest on home equity loans may be tax-deductible if used for home improvements. The same applies to HELOC interest if funds improve your home. Using funds for other purposes might not qualify for deductions. Keep receipts and consult a tax advisor to be sure.

Credit: www.experian.com

Usage Scenarios

Choosing between a home equity loan and a HELOC depends on how you plan to use the money. Each option fits different needs and spending habits. Understanding common usage scenarios helps pick the right choice.

Home Renovations

Home equity loans work well for big projects with fixed costs. You get a lump sum upfront. This helps pay contractors and buy materials. The loan has a set interest rate and monthly payment. It is easier to budget for long renovations.

HELOCs suit ongoing or smaller repairs. You borrow money as needed. This is good for projects that change over time. You only pay interest on what you use. Flexibility is a key benefit here.

Debt Consolidation

Home equity loans can pay off multiple debts at once. This simplifies payments with one monthly bill. The fixed rate often lowers interest costs. It helps reduce financial stress quickly.

HELOCs also work for debt consolidation but need careful use. You can borrow and repay repeatedly. This requires discipline to avoid more debt. It is better for those who manage money well.

Emergency Expenses

HELOCs are ideal for emergencies. Access funds anytime during the draw period. Use only what you need for sudden costs. This keeps interest charges low.

Home equity loans are less flexible for emergencies. You get a lump sum and must pay interest on all. Not the best choice for unexpected or small needs.

Risks And Benefits

Choosing between a home equity loan and a HELOC means understanding their risks and benefits. Both let you borrow using your home’s value. Each has unique features that affect your finances and credit. Knowing these helps you make a smart choice.

Both options can help with big expenses. Yet, they come with financial risks you must consider. The right choice depends on your money habits and goals.

Financial Flexibility

Home equity loans give a lump sum with fixed payments. You pay the same amount each month. This makes budgeting easier. HELOCs work like credit cards with a borrowing limit. You borrow money as needed and pay interest only on what you use. HELOCs offer more flexibility but can lead to overspending.

Impact On Credit

Both loans affect your credit score. Using a home equity loan may increase your debt at once. HELOCs may cause credit score changes if balances rise. Timely payments improve credit. Late payments hurt your credit and raise costs. Keep track of your borrowing and payments.

Risk Of Foreclosure

Both loans use your home as security. Missing payments can lead to foreclosure. This means losing your home. Borrow only what you can repay. Understand the terms before signing. Protect your home by staying current on payments.

Qualification Criteria

Qualifying for a home equity loan or HELOC requires meeting specific rules. Lenders check your financial health to decide if you can borrow money. Understanding these rules helps you prepare your application. Focus on credit score, home value, and income. These factors show lenders your ability to repay the loan.

Credit Score Requirements

Lenders want to see a good credit score. Usually, a score of 620 or higher works. Higher scores get better interest rates. Scores below 620 may lead to denial or high costs. Check your credit report before applying. Fix errors and pay down debts to improve your score.

Home Equity Calculation

Equity means the home’s market value minus what you owe. Lenders use this number to decide your loan size. Most allow borrowing up to 80% to 85% of your equity. For example, if your home is worth $300,000 and you owe $200,000, you have $100,000 in equity. You could borrow up to $80,000 to $85,000.

Income Verification

Lenders verify your income to ensure you can pay back. They ask for pay stubs, tax returns, or bank statements. Consistent income improves your chances. Self-employed borrowers may need extra documents. Low income can reduce how much you borrow or lead to denial.

Making The Right Choice

Choosing between a home equity loan and a HELOC can feel confusing. Each option fits different needs and situations. Understanding your financial goals and loan details helps you pick the best one. Getting advice from experts adds clarity. This section breaks down key points to guide your choice.

Assessing Financial Goals

Start by thinking about your money plans. Need a lump sum or flexible funds? Home equity loans give a fixed amount at once. HELOCs let you borrow as you go. Consider how you will use the money. Also, think about your repayment ability. Clear goals make the decision easier.

Evaluating Loan Terms

Look closely at interest rates and repayment schedules. Home equity loans often have fixed rates and set payments. HELOC rates may change and payments can vary. Check fees for both options. Understand how long you have to repay. Knowing terms helps avoid surprises later.

Consulting Financial Advisors

Talk to a financial advisor for expert advice. They can explain loan details simply. Advisors help match loans to your situation. They also show risks and benefits clearly. Getting professional help reduces stress and boosts confidence in your choice.

Credit: www.citizensbank.com

:max_bytes(150000):strip_icc()/dotdash_Final_Home_Equity_Loan_vs_HELOC_What_the_Difference_Apr_2020-01-af4e07d43f454096b1fbad8cfe448115.jpg)

Credit: www.investopedia.com

Frequently Asked Questions

What Is The Difference Between A Home Equity Loan And Heloc?

A home equity loan provides a lump sum with fixed interest. A HELOC offers a revolving credit line with variable rates. Choose based on your repayment comfort and funding needs.

When Should I Choose A Home Equity Loan?

Pick a home equity loan if you need a one-time, fixed amount. It’s ideal for large, predictable expenses like home renovations or debt consolidation.

How Does A Heloc Work For Ongoing Expenses?

A HELOC lets you borrow repeatedly up to a credit limit. You pay interest only on what you use, making it flexible for ongoing or unexpected costs.

Are Interest Rates Higher On Helocs Or Home Equity Loans?

HELOCs usually have variable rates, which can rise over time. Home equity loans have fixed rates, offering stable monthly payments. Rate choice depends on your risk tolerance.

Conclusion

Choosing between a home equity loan and a HELOC depends on your needs. A home equity loan offers a fixed amount and steady payments. A HELOC gives flexible borrowing and variable rates. Think about your budget and how you plan to use the money.

Both have pros and cons to consider. Take your time to compare terms and costs. Speak with a lender to get advice for your situation. Making the right choice helps you manage your finances better and avoid surprises later.