Are you wondering whether you should remortgage or opt for equity release? Making the right choice can have a big impact on your finances and future.

Both options can help you unlock money tied up in your home, but they work in very different ways. Choosing the wrong path could cost you more than you expect or limit your options later on. You’ll discover the key differences between remortgaging and equity release.

By the end, you’ll feel confident about which option suits your needs best and how to take the next step. Keep reading to make a decision that truly benefits you.

Comparing Remortgage And Equity Release

Deciding between remortgaging and equity release can affect your finances greatly. Both options let you access money tied up in your home. Each has unique features and suits different needs. Understanding how they work helps you choose wisely.

Basics Of Remortgaging

Remortgaging means switching your mortgage to a new deal. You might get a lower interest rate or better terms. It can reduce monthly payments or free up cash. You still repay the loan in full over time. Your home acts as security for the mortgage.

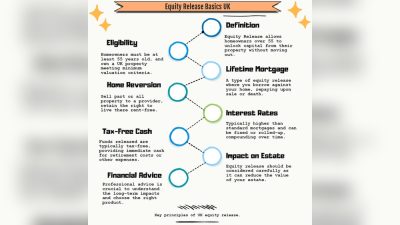

How Equity Release Works

Equity release lets older homeowners get money from their home value. You borrow against your property without moving out. The loan plus interest repays after you die or move permanently. No monthly payments are needed during your lifetime. It reduces the inheritance left to your heirs.

Key Differences

Remortgaging requires regular repayments on loan and interest. Equity release delays repayment until later in life. Remortgage suits people who want to lower costs or borrow more. Equity release fits those who need cash but cannot pay monthly. Remortgage may need good credit and income. Equity release depends on age and home value.

Credit: everyinvestor.co.uk

When Remortgaging Makes Sense

Remortgaging can help you save money or change your loan to fit your needs better. It is a good choice when your current mortgage is costing too much. You may also want to remortgage to get extra cash from your home. Knowing when to remortgage helps you make smart financial decisions.

Lower Interest Rates

Interest rates change over time. If rates have dropped since you took your mortgage, remortgaging can lower your monthly payments. Paying less interest means saving money each month. This option works best if your credit score is good.

Changing Loan Terms

You can adjust your loan length by remortgaging. Shortening your term helps you pay off your home faster. Lengthening it lowers monthly payments but may increase total interest. Changing terms suits your current financial situation.

Accessing Home Equity

Remortgaging can give you cash from your home’s value. This money can help with home improvements or other needs. It lets you borrow more without selling your house. Use this option if you want funds at a lower cost.

Situations Favoring Equity Release

Equity release can suit certain homeowners better than remortgaging. It works well for older people who want to use their home’s value without monthly payments. This option gives cash based on property value and age. It fits specific financial and lifestyle needs.

Understanding when equity release fits helps make smart choices. Some situations clearly favor this option over remortgages. Here are key examples.

Retirement Income Needs

Equity release helps people with fixed or low retirement incomes. It provides extra money to cover living costs. This cash comes from home value, not salary or savings. Good for those wanting more spending money without working more.

No Monthly Repayments

This option does not require monthly loan payments. The loan and interest repay only when the house sells. No monthly stress on budgets. Ideal for people who want to keep monthly bills low and stable.

Age And Property Requirements

Most equity release plans need you to be 55 or older. The property must be your main home and meet certain rules. Larger homes or those in good condition often qualify. This makes equity release possible for many older homeowners.

Financial Implications To Consider

Choosing between remortgaging and equity release affects your finances in many ways. Understanding these effects helps you make the right choice. Think about all costs, the impact on your family, and taxes. Each factor shapes your financial future differently.

Costs And Fees

Remortgaging usually has setup fees and early repayment charges. These fees can add up quickly. Equity release also has costs like arrangement fees and legal charges. Some products have higher interest rates. Check all fees before deciding. Small costs can become large over time.

Impact On Inheritance

Equity release reduces the value of your estate. Your family will inherit less after you pass away. Remortgaging does not reduce your home’s value directly. You keep more to pass on with remortgaging. Think about how much you want to leave behind. This choice affects your loved ones financially.

Tax Considerations

Money from equity release is usually tax-free. It does not count as income. Remortgaging does not affect your taxes directly. Interest on remortgaged loans is not tax-deductible for most people. Talk to a tax advisor to understand your situation. Taxes can change how much money you keep.

Risks And Limitations

Choosing between remortgaging and equity release involves risks and limits. Understanding these helps make a safer choice. Each option affects your finances and future differently.

Effect On Benefits And Allowances

Equity release can reduce your income-based benefits. This happens because releasing money counts as income or savings. Remortgaging usually does not affect benefits directly. Check with a benefits advisor before deciding.

Potential For Negative Equity

Negative equity means you owe more than your home is worth. It can happen if house prices fall after remortgaging or equity release. Some equity release plans protect against this risk. Remortgages do not always offer this safety.

Flexibility And Restrictions

Remortgages often have fixed terms and repayment rules. This limits changing your loan early without fees. Equity release offers fewer repayment demands but reduces your home’s inheritance. Both options require careful planning for future needs.

Credit: www.nerdwallet.com

Steps To Make A Smart Choice

Deciding between remortgaging and equity release takes careful thought. Follow clear steps to choose wisely. Understand your needs. Know your options. Compare details. This helps avoid costly mistakes and ensures financial comfort.

Assessing Your Financial Goals

Start by listing what you want to achieve. Need extra cash or lower monthly payments? Planning for retirement or funding home improvements? Your goals guide the best choice. Write down your short and long-term aims. This shows which option fits best.

Seeking Professional Advice

Talk to a financial expert. They explain complex terms and risks. They look at your whole financial picture. Professionals suggest the safest, most suitable path. Avoid decisions based on guesswork or pressure.

Comparing Offers And Terms

Gather quotes from several lenders or providers. Check interest rates, fees, and repayment rules carefully. Look beyond monthly costs. Consider total repayment amounts and flexibility. Clear comparisons reveal the best deal for your needs.

Credit: boonbrokers.co.uk

Frequently Asked Questions

What Is The Main Difference Between Remortgage And Equity Release?

Remortgage replaces your current mortgage with a new one, often for better rates. Equity release allows homeowners aged 55+ to access home equity without moving. Remortgage requires monthly repayments, while equity release usually doesn’t until you sell or pass away.

When Should I Consider Remortgaging Instead Of Equity Release?

Consider remortgaging if you want lower interest rates or to reduce monthly payments. It suits those who can still afford repayments and aim to retain full home ownership. Equity release is better for accessing cash without monthly repayment pressure.

What Are The Risks Of Choosing Equity Release Over Remortgage?

Equity release can reduce inheritance and increase interest over time. It may affect benefits and future house sale proceeds. Remortgage risks include affordability and potential fees but keeps your home ownership intact.

How Does Remortgage Impact My Credit Score Compared To Equity Release?

Remortgaging may temporarily lower your credit score due to credit checks. Equity release usually doesn’t affect credit scores since it’s not a loan requiring monthly payments. Both impact finances, but remortgage affects credit history more directly.

Conclusion

Choosing between remortgaging and equity release depends on your needs. Think about your financial goals and how much money you need. Remortgaging lowers your monthly payments or gets better rates. Equity release gives cash but affects your home’s value. Talk to a financial adviser before deciding.

Understand all costs and risks involved. Make sure your choice fits your long-term plans. Take your time and choose what feels right for you. Your home and money deserve careful thought.