Thinking about buying another house but unsure how to fund it? You might have heard about using a home equity loan as a way to unlock cash from your current home.

But can you really use that money to buy a second property? Understanding how this works could save you time, money, and stress. You’ll discover exactly what a home equity loan is, how it can help you invest in another house, and what important factors to consider before taking this step.

Keep reading to find out if tapping into your home’s value is the right move for your next big purchase.

Home Equity Loan Basics

Understanding home equity loans is important before using one to buy another house. These loans let homeowners borrow money using the value of their current home. This section explains the basics of home equity loans. Learn what they are and how they work.

What Is A Home Equity Loan

A home equity loan is money borrowed against your home’s value. You get a lump sum that you repay over time with fixed interest. The loan uses your house as security. It is different from a mortgage because you already own the home. The loan amount depends on your home’s current value minus what you owe.

How Home Equity Loans Work

You apply for a home equity loan through a bank or lender. The lender checks your home’s value and your credit. They decide how much money you can borrow. You receive the money all at once. Then, you pay back the loan in monthly payments. The interest rate is usually fixed, so payments stay the same. Missing payments can risk losing your home.

Credit: www.pacaso.com

Using Home Equity Loans For Property Purchase

Using home equity loans to buy another house is a common strategy for many homeowners. This loan lets you borrow money using your current home’s value. You can use this money as a down payment or to pay for the full price of a new property. This option can help you invest in real estate without selling your current home.

Understanding the rules and benefits of home equity loans is important before making a decision. Knowing who qualifies and what advantages these loans offer helps you plan better.

Eligibility For Buying Another House

To qualify for a home equity loan, you must have enough equity in your current home. Lenders usually require at least 15% to 20% equity. Your credit score and income also matter. A good credit score increases your chances of approval. Lenders check your ability to repay the loan. Having a steady income helps show you can handle two loans.

Some lenders may limit how much you can borrow based on your home’s value and your debts. Make sure to check your loan-to-value ratio. It should be within the lender’s limits to qualify.

Advantages Of Using Home Equity Loans

Home equity loans often have lower interest rates than other loans. This makes borrowing cheaper. The loan amount is usually large, allowing for bigger property purchases. You get a fixed interest rate, so your monthly payments stay the same. This helps with budgeting.

Using a home equity loan can speed up the buying process. You get cash upfront, which can make your offer more attractive to sellers. Also, interest payments on home equity loans may be tax-deductible. Check with a tax advisor to confirm this for your situation.

Risks And Considerations

Using a home equity loan to buy another house has risks to consider. These risks affect your money and credit health. Understanding them helps you make a smart choice. Think about how this loan fits into your overall finances.

Potential Financial Risks

A home equity loan uses your current home as collateral. Missing payments can lead to losing your home. Interest rates might rise, increasing monthly payments. You may face higher debt than expected. The new house might not increase in value. This situation can make it hard to sell or rent. Budget carefully to avoid financial strain.

Impact On Credit And Debt

Taking a home equity loan adds to your debt load. This increase can lower your credit score. More debt may limit your ability to borrow later. Late payments also harm your credit rating. A lower credit score means higher loan costs. Track payments closely to protect your credit. Use the loan only if you can manage extra debt.

Credit: retipster.com

Alternative Financing Options

Buying another house can require extra money. Using a home equity loan is one way to get funds. There are other options too. These alternatives might suit your needs better. Understanding them helps you make smart choices.

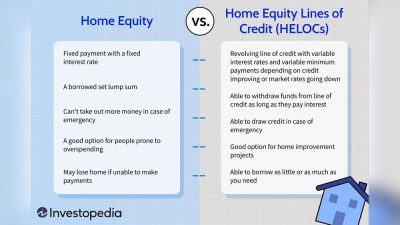

Home Equity Line Of Credit (heloc)

A HELOC lets you borrow money against your home’s value. It works like a credit card with a set limit. You borrow what you need and pay interest only on that amount. It offers flexibility for buying a second house. You can use it multiple times during the draw period. Interest rates are often lower than other loans. Payments can vary, so budgeting is important.

Traditional Mortgage Loans

Traditional mortgage loans are common for buying homes. They offer fixed or variable interest rates. You borrow a large sum and repay over many years. These loans usually have lower interest rates than home equity loans. Qualification depends on credit score, income, and debt. Down payments are often required, usually around 20%. This option works well for long-term financing. It spreads out payments, making them more manageable.

Steps To Apply For A Home Equity Loan

Applying for a home equity loan involves clear steps. Understanding these steps helps you prepare and apply smoothly. The process starts with meeting qualifying criteria. Then, you move on to the application process.

Qualifying Criteria

Lenders check your credit score and income. They want to see if you can repay the loan. Your home’s value matters too. The amount you owe on your mortgage affects approval. Lenders usually allow borrowing up to 80% of your home’s value minus what you owe.

Stable income and good credit increase your chances. Some lenders may require proof of income. Your debt-to-income ratio is also important. Lower debt means better chances to get the loan.

Application Process

Start by gathering important documents. These include proof of income, tax returns, and details about your home. Next, fill out the loan application form. Provide accurate and complete information.

The lender will then appraise your home. This confirms its current market value. After appraisal, the lender reviews your application. They check your credit and financial details again. If approved, you receive a loan offer with terms.

Review the offer carefully before signing. Once signed, the loan funds are released. You can use the money to buy another house or for other needs.

:max_bytes(150000):strip_icc()/MillRate-20ac0b75a5a24c1ba2a100d7b625a6b3.jpeg)

Credit: www.investopedia.com

Tips For Managing Multiple Properties

Owning more than one property can be rewarding but needs careful management. Many people use a home equity loan to buy another house. Handling multiple homes means planning finances and understanding taxes well. Good management helps avoid stress and extra costs. Here are key tips to keep your properties running smoothly.

Budgeting And Cash Flow

Track all income and expenses for each property carefully. Set aside money for repairs and unexpected costs. Ensure rent or income covers the loan payments and bills. Keep a clear record to avoid surprises. Use separate accounts to manage funds for each home. This helps see where money goes and what you earn.

Tax Implications

Owning multiple properties affects your taxes in different ways. You may deduct mortgage interest and repair costs. Rental income must be reported and taxed. Know the rules for depreciation and capital gains tax. Consult a tax professional to avoid mistakes. Proper filing can save money and prevent penalties.

Frequently Asked Questions

Can A Home Equity Loan Finance A Second Property?

Yes, you can use a home equity loan to buy another house. It provides funds based on your current home’s value. However, lenders consider your income and creditworthiness before approval. This option can help with down payments or full property purchase.

What Are The Risks Of Using Home Equity For Buying?

Using home equity to buy a house risks your current home as collateral. If you default, you could lose your property. Interest rates may also be higher than primary mortgages. Careful financial planning is essential before leveraging your home equity.

How Does A Home Equity Loan Differ From A Mortgage?

A home equity loan is a second loan using your home’s value. It usually has a fixed interest rate and term. A mortgage is the primary loan to buy your home. Both loans impact your monthly payments and credit score.

Can I Get A Home Equity Loan With Bad Credit?

Getting a home equity loan with bad credit is challenging. Lenders prefer good credit scores for approval. Higher interest rates or stricter terms may apply if approved. Improving credit before applying increases your chances and loan affordability.

Conclusion

Using a home equity loan to buy another house can work for some people. It offers extra money without selling your current home. But it also adds risk since your home is the loan’s security. Think about your budget and future plans carefully.

Talk to a financial expert to see if this fits your needs. Weigh the pros and cons before making a choice. This way, you can make a smart decision about using your home equity.